24 Things to Watch in Lift-Served Skiing in 2024

Megapass evolution, consolidation, sky-high lift ticket prices, climate wars, the rise of indoor skiing, lost ski area comebacks, and more.

In 2023, I tried predictions, which went about as well as one could predict. Which is to say, poorly. There’s a reason I don’t gamble, and a reason I’d avoided the crystal-ball exercise for The Storm’s first three years (and 2020 should have validated that posture as the correct one). So let’s reframe this for 2024: rather than saying “this is what will happen,” I’ll just wave broadly toward a bunch of things that I’ll be locked onto this year. With probably half of them, nothing will change. But the ones that do change could do so in a big way. Maybe. Let’s see:

MULTI-MOUNTAIN PASSES

1) Will big mountains switch teams?

In 2019, Arapahoe Basin fled a decade-long Epic Pass partnership and landed on the Ikon and Mountain Collective passes. In 2022, Sun Valley and Snowbasin followed, returning to Mountain Collective and joining Ikon for the first time after three years partnering with Vail. We all expected Telluride to follow, but then they didn’t.

Vail, with 42 owned mountains (to Alterra’s 18), needs fewer friends on Epic than their biggest rival has collected on Ikon. But it could use a few more. Epic Pass unit sales growth (by units sold), slowed to its lowest levels ever in 2023, even with prices sitting substantially below Ikon’s. An analysis of competing lineups suggests a reason why: Ikon has collected the greatest resort roster in the history of skiing, with nearly three times as many ski areas in the western U.S. as Epic.

Which is great for skiers and likely great for Ikon Pass sales. However. Everyone has to eat from the same pot, and right now, there are a lot of spoons. At some point, Vail might go New York baseball on the game, bust out the checkbook, and start luring some of these headliners off the Ikon marquee. Don’t think it could happen? The 108-year-old Pac 12 Conference is about to disintegrate as member schools chase amazing paychecks across the Mississippi. If Vail wants to start buying partners, it probably can.

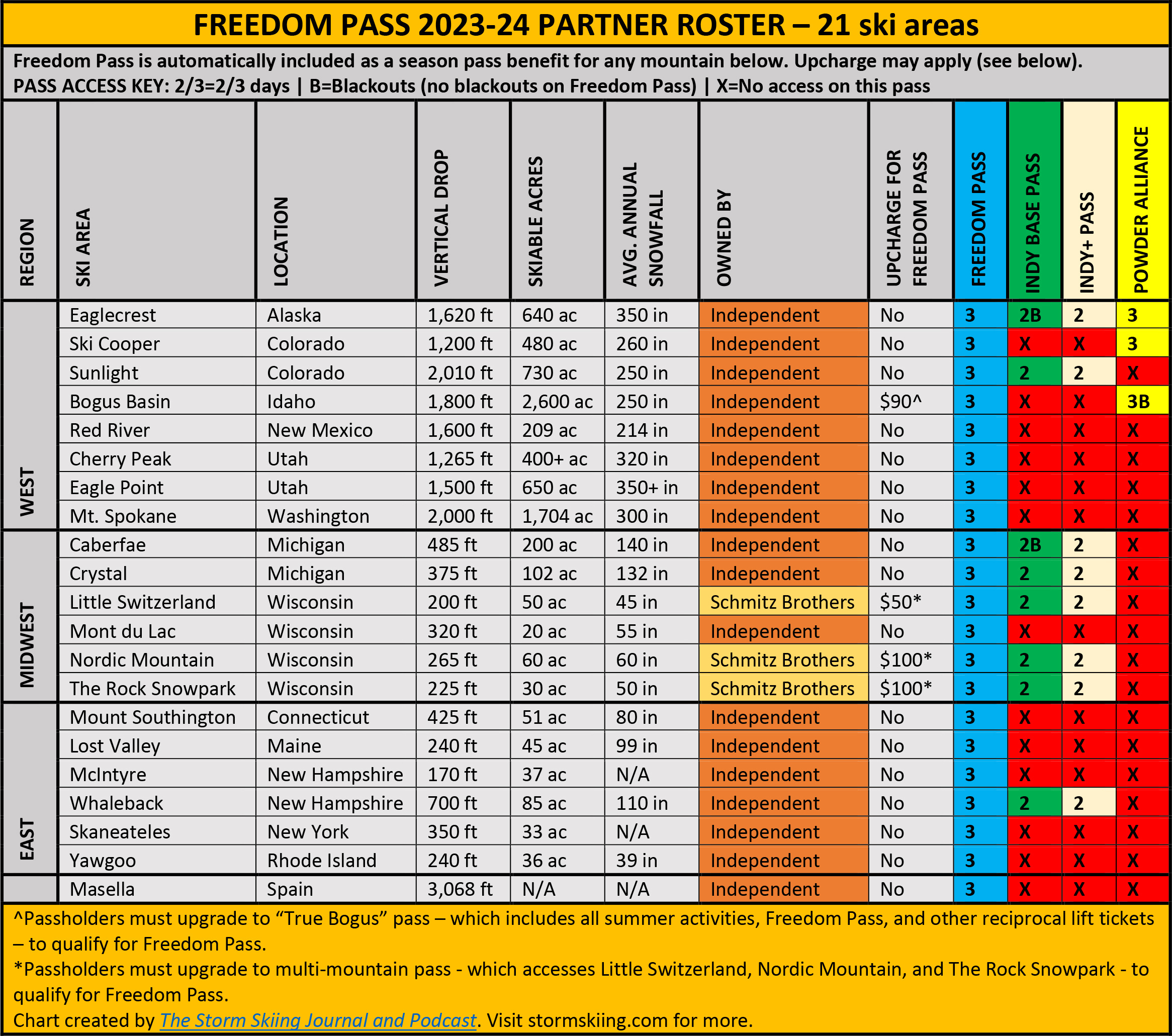

2) Will Freedom Pass die on the hill?

Of the large multimountain pass coalitions, Freedom Pass is the least appealing, with far-flung mountains, few marquee partners, and a limited number of tangible benefits for season passholders, who are eligible for three free lift tickets at each partner ski area:

The best eastern mountains have all fled – big, snowy Greek Peak bounced after someone let tiny nearby Skaneateles in the door (granting those passholders three free GP tickets). And I confirmed yesterday with Black Mountain, New Hampshire owner John Fichera that he had withdrawn his ski area from the coalition as well. That makes 85-acre, 700-vertical-foot Whaleback the largest Northeast ski area on the pass.

Yes, there are still some fun exchanges on there (Crystal-Caberfae, Sunlight-Ski Cooper, Southington-Yawgoo), but mostly this is a strange stew. The western mountains are solid but far-flung. Administratively, the thing is a mess – the managing ski area has changed four times in at least as many years (by contrast, Mountain High has managed Powder Alliance from its outset, more than a decade ago).

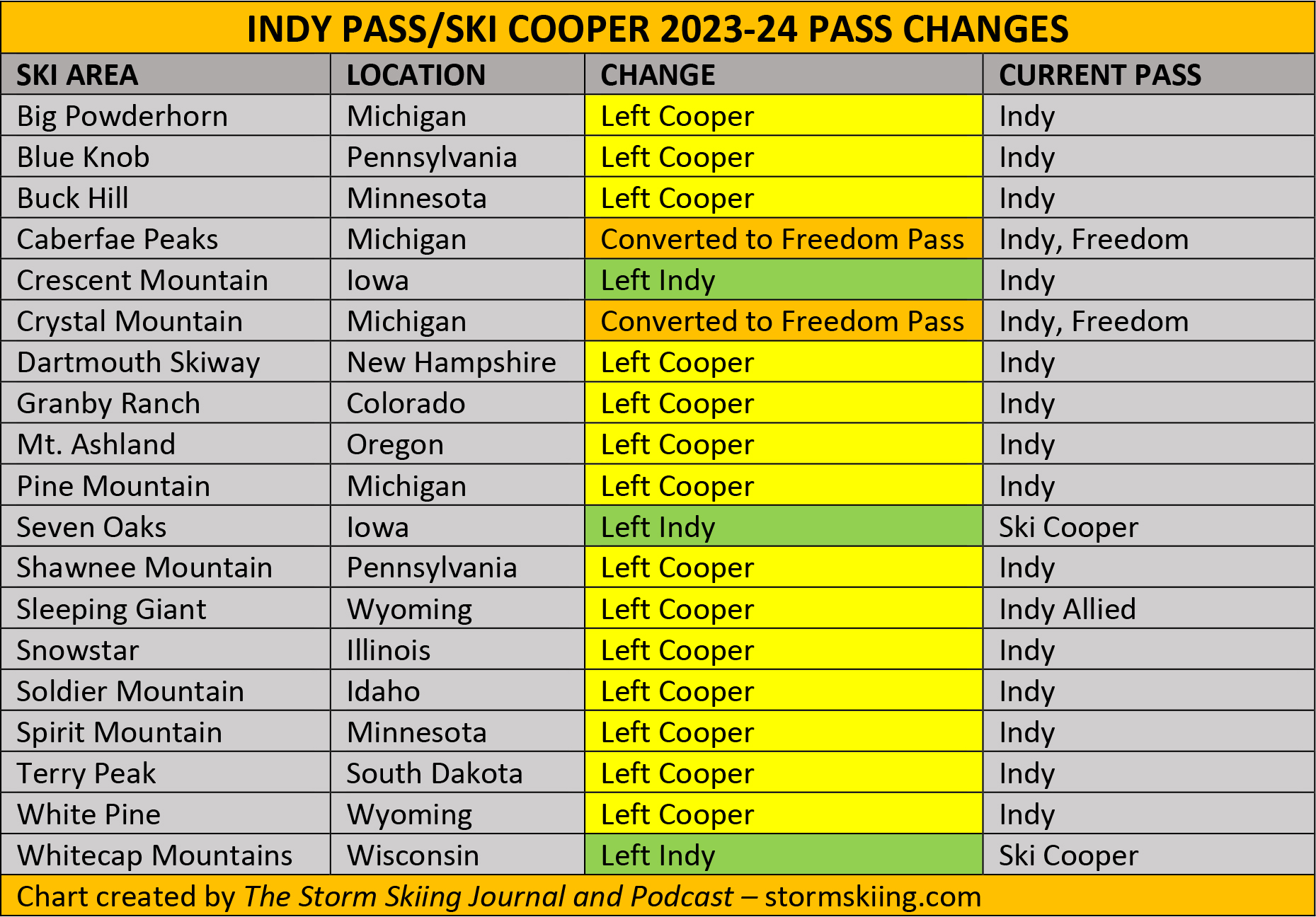

But what could really kill Freedom Pass is Indy Pass, which, last summer, told its partners to ditch their reciprocal agreements with Ski Cooper, whose $379 season pass acted as a de facto national pass. Most of them sided with Indy and that pass’ per-visit payout. But Indy limited its ultimatum to partners who had not joined Freedom Pass or Powder Alliance (both of which Cooper belongs to), intimating that it would deal with those coalitions next year. It’s next year, and if Indy tells its eight Freedom Pass partners to choose, this thing may finally fall apart for good.

3) Will super-discount season passes survive?

Indy’s offensive against Ski Cooper, while somewhat off-putting to some of its partners, was remarkably effective. Of the 19 non-Freedom/non-Powder Alliance ski areas that the two coalitions shared when Ski Cooper’s pass went on sale in July, 14 left Cooper and only three left Indy – and one of those was Whitecap, an Allied Indy resort that was not benefitting from per-visit paychecks. Two neighboring Michigan mountains – Caberfae and Crystal – skirted the issue by joining Freedom Pass. Here’s how it all broke down:

Which sets up this question: what of the other super-discounted, single-mountain season passes that act as de-facto national discount cards? There are two, in particular, that may draw Indy’s ire: Mount Bohemia, Michigan and Mont du Lac, Wisconsin, each of which sell a $99(-ish) season pass loaded with dozens of reciprocal partners.