Could This Regional Ski Pass Become Skiing’s Next National Megapass?

How the Power Pass could aggressively expand its footprint beyond the Southwest

A National Power Pass would combine Indy Pass’ ethos with Ikon Pass’ blueprint

Somewhat overlooked in the rapid consolidation of the continent’s megaresorts onto the Epic and Ikon passes is the proliferation of the regional ski pass. New Hampshire’s White Mountain Super Pass delivers unlimited access to Cannon, Waterville Valley, Bretton Woods, and Cranmore for $1,259 (early-bird price was $1,099). The Berkshire Summit Pass is good at Berkshire East, Catamount, and Bousquet, all in Massachusetts, for $559 (early bird $499). New York offers several options: Labrador and Song share a pass ($499 early-bird price; not currently on sale), as do Greek Peak and Toggenburg ($745/$630 early bird), and of course state-owned Whiteface, Gore, and Belleayre share the NY Ski3 Pass ($809 until Aug. 18).

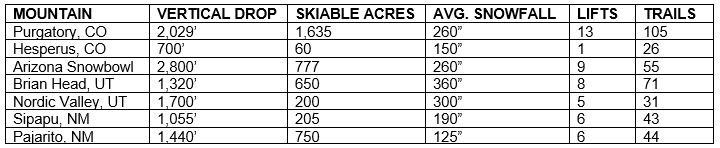

There are plenty more passes like those, and not just in the Northeast. One of the most intriguing of these is Mountain Capital Partners’ (MCP) Power Pass, which grants skiers access to seven ski areas across the Southwest for $799. Here’s a brief overview of their mountains:

Passholders also get three no-blackout days each at Sundance Utah and Copper Mountain, Loveland, and Monarch Mountain in Colorado. And the Power Pass grants unlimited access to Spider Mountain, Texas, which MCP claims is the only year-round lift-served MTB park in the country. As with the Epic and Ikon Passes, lower-priced Power Pass tiers offer more restricted access.

So what? By Western standards, these are not huge mountains. The largest – Purgatory – is the 12th biggest ski area in Colorado by skiable acres, and ranks 17th in the state by vertical drop, below Aspen’s homey Buttermilk. And compared to their peer mountains in the region, there’s nothing special about the snowfall totals, trail footprints, or lift networks.

But what’s special about the Power Pass is not the mountains themselves, but how they came together and the spirit that animates them. MCP is perhaps the most improbable conglomerate in skiing, a collection of mostly (at the time of acquisition) under-developed mountains united by the swashbuckling James Coleman, who decided on a high school ski trip that he wanted to own a ski area and didn’t stop until he had saved enough money to buy a ski area. That was Sipapu, in 2000. He added Pajarito in 2014, Purgatory and Arizona Snowbowl in 2015, Hesperus in 2016, Nordic Valley (as manager) in 2018, and Brian Head in 2019. MCP also owns Purgatory Snowcat Adventures, the largest Cat skiing operation in Colorado, and the currently shuttered Elk Ridge ski area in Arizona (permitting issues have kept the small mountain closed).

Once MCP acquires a mountain, they aggressively invest. They’ve pumped $40 million into their portfolio so far, and recently unveiled a mammoth, 15-year master plan for Arizona Snowbowl. Much of this goes to new lifts and snowmaking. As Devon O’Neil wrote in Outside:

“To counter the threats of drought and warmer winters, Coleman makes sure his resorts open early and stay open via manmade snow, invests in modern base-area amenities, upgrades chairlift infrastructure as quickly as he can, and focuses on providing all kinds of terrain, from steeps to the bunny hill.”

Coleman himself is the catalyst here, roving his mountains, chainsaw in hand, thinning trees or rigging up Goldbergian snowmaking contraptions. He is a skier, crafting skier’s mountains.

“My constant mantra is that the skiing comes first,” Coleman told Jason Blevins, then at the Denver Post, in 2016. “That’s why we are here. You can stay at condos at a ski mountain, … but the skiing is the reason those condos are here. All the lodges and restaurants, those things are all important, but the skiing has got to be first.”

Megapass potential

There was nothing inevitable or intuitive about the advent of the megapass. For decades, skiing had no such thing. Vail’s insight in 2008 was to combine its mountains – at the time, Vail, Beaver Creek, Keystone, Breckenridge, Heavenly – onto a single pass. Alterra’s insight was that large independents were getting their asses handed to them by the Epic Pass and needed to join forces (they had a good foundation to build off of with the Mountain Collective and M.A.X. passes). And Indy Pass founder Doug Fish’s insight was that a national ski coalition could be built on regional destinations, without the apex mountains that even non-skiing folks have heard of.

These passes have been amazing for skiers and amazing for the ski industry. They have forced independent operators to innovate and add more value to their passes, and they have created a sense of belonging among passholders that enables and encourages frequent skiing.

But scanning the national pass landscape, there is a lot of room left to grow. According to the NSAA, 470 U.S. ski areas operated during the 2019-20 season, the most recent for which statistics are available. You can ski 35 of them on the Epic Pass, 36 on the Ikon Pass, and 65 on the Indy Pass. The Mountain Collective has a lot of crossover with the Ikon Pass, plus Grand Targhee. That means 137 mountains are spoken for by one of the four national ski passes – but 333 of them are not. Indy plans to top out around 90 partners. Alterra and Vail can’t – and don’t want to – buy everything. Mountain Collective has only so far been interested in flagship destinations.

That means there is an enormous opportunity for a fifth national pass. Boyne or Powdr could have anchored this, but they chose to join forces with Alterra. MCP could build an Ikon Pass-like coalition, with unlimited access to its owned mountains and limited days at partner ski areas (the three days it already offers to partner areas would be sufficient), using an Indy Pass blueprint that builds on regional destinations.

A national Power Pass could look something like this:

West: build off the existing partner list (Monarch, Loveland, Sundance, Copper if Powdr and Alterra would allow it), by adding three days each at Powder Alliance partners Angel Fire, New Mexico; Bogus Basin, Idaho; Mount Hood and Timberline, Oregon; and Mountain High and Sierra-at-Tahoe, California. Convince some combination of Sunlight, Ski Cooper, Wolf Creek, Diamond Peak, Mt. Rose, Homewood, Bridger Bowl, Whitefish to join you, and that takes care of the West. The majority of those are probably too small to interest Vail or Alterra, but would be major wins for Indy or anyone else. Even if Indy and MCP divided these, both would still be substantial offerings.

Northeast: New York’s three state-owned ski resorts were part of the M.A.X. Pass, and would be an enormous regional draw even as limited partners. Holiday Valley or Bristol could anchor western New York. The Fairbank Group’s three resorts – Bromley in Vermont, Jiminy Peak in Massachusetts, and Cranmore in New Hampshire – would make an excellent New England anchor, especially if they were supplemented by Smugglers’ Notch, Mad River Glen, or Bretton Woods. Former M.A.X. Pass partner Wachusett has one of the strongest partner networks in the Northeast, and would fit right in. Finally, strike a deal with Pacific Group Resorts, which would add not only the criminally overlooked Ragged Mountain, New Hampshire, but Powderhorn in Colorado, plus Mid-Atlantic ski areas Wintergreen in Virginia and Wisp in Maryland.

Midwest: This would be a tough region, since Indy has already established the strongest position of any national pass throughout Minnesota, Wisconsin, and Michigan. A good starting point would be Wisconsin resorts, which owns several small and busy suburban ski resorts and the outstanding Searchmont, just across the Michigan border in Ontario. Taking a cue from Vail, these little Midwest hills could feed a steady pipeline of skiers to the West. And there is still room to grow, particularly in Michigan, where Marquette Mountain, Big Snow’s Indianhead and Blackjack, and Nub’s Nob all remain unaffiliated.

This is assuming there is no crossover with the Indy, Ikon, or Mountain Collective passes (Vail has made clear that Epic Pass deals are exclusive). But there are clearly enough big, interesting mountains left in the United States to fill another national pass. And as the Epic and Ikon passes grow in popularity, so too, probably, will their liftlines. It’s too hard to build new ski resorts in the United States, but we have lots of capacity to push skiers around to the ones that are underutilized now.

Could it work?

This is all pure speculation on my part, based on the growing popularity of multipasses and skiers’ evolving expectations of multi-mountain access with a season pass purchase. But I did reach out to MCP to see if they’ve explored growing the Power Pass beyond their Southwest base.

“We have talked about someday entering into an agreement with mountains that are non-MCP mountains, although at this point, those have been purely high-level brainstorms,” said Stacey Glaser, senior marketing director at MCP.

The Power Pass has actually gone in the opposite direction, trimming reciprocal agreements as it’s grown its core. “We still have a few traditional reciprocal agreements in place,” Glaser said. “These are your typical three-days-for-three-days exchange. We've really scaled this back over the years, however. We feel there's tremendous value within our own collective and want to continue to encourage our guests to ski our mountains.”

The potential for rapid expansion is there if they want it. The Indy Pass didn’t exist two years ago. Now it has 68 partner mountains, with more coming before ski season. The Ikon Pass is just three years old. The ski world is evolving rapidly, and the megapass is proven as a business concept – Vail’s global empire is built around the genius of the Epic Pass. Like snowmaking or high-speed lifts or e-commerce, more ski areas will want in on a concept that’s proven to work at attracting skiers, stabilizing revenue, and increasing a mountain’s national and regional profile.

Ikon Pass crushes it with new interactive map

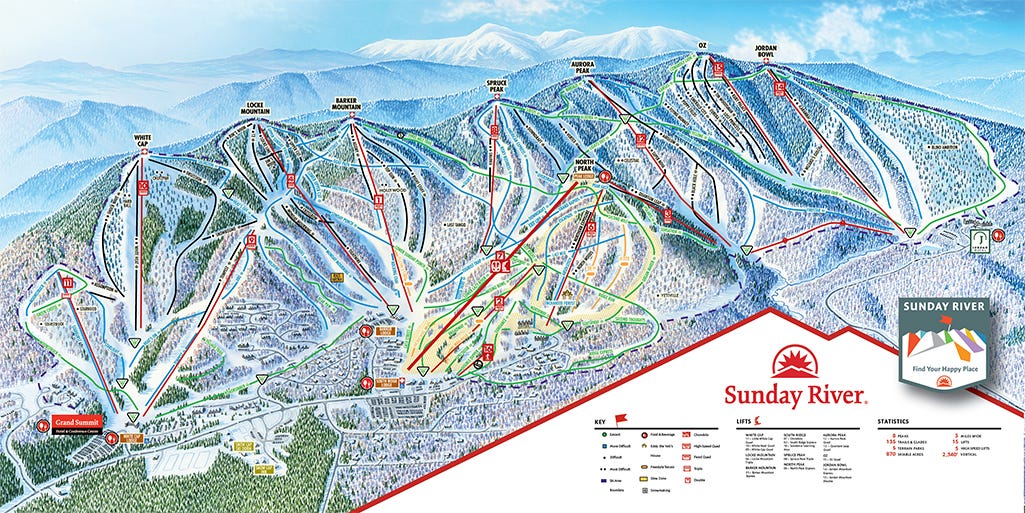

I love trailmaps. They are indispensable on the mountain. Tangible artifacts of a visit, they are often beautiful. The walls of my laundry room are covered with trailmaps I’ve collected over the past 25 years.

But they are an illusion, a flattening of natural mountain contours to fit the perspective of two-dimensional paper. It’s hard to appreciate how vastly most trailmaps differ from the ski area they represent until you’re on the mountain. On paper, valleys shrink. Three faces fold out into one. Entire forests and cliff bands evaporate.

Which is why the new interactive Ikon Pass destination map is so incredible. You can click into a 3D perspective of any Ikon Pass destination, clicking, scrolling, and zooming into and around the mountain. The sense of perspective is astonishing. Compare this standard trailmap of Sunday River:

To the 3D view on the Ikon Pass site:

This is the best multi-resort map in skiing. Vail’s Epic Pass map requires too much clicking around, and the trailmaps are buried on the individual resort sites. Mountain Collective just has a static image. Indy’s map is hard to use, with no hover feature indicating which resorts correspond with which dots, and individual ski area info dropped seemingly at random below (rather than organized by states, for example). Powder Alliance actually has one of the flashier maps, but it still requires too much clicking. Ikon got this one right.

Speaking of megapass speculation

Summit Daily ran an interesting piece yesterday that riffed on Vail CEO Rob Katz’s comments on possible acquisitions during the company’s recent earnings call:

Headed into the summer with $1.3 billion cash on hand and no dividend yet planned for shareholders, discipline is the word as executives decide if and how to spend the company’s excess capital.

“We will continue to be disciplined stewards of our capital, with a focus on high-return capital projects, continuous investment in our people and strategic acquisition opportunities,” Katz said on the call with investors.

What could that mean for the Northeast in particular?

Benjamin Chaiken, a Wall Street Analyst at Credit Suisse, asked Vail Resorts if the strength of pass sales in the Northeast could lead to more acquisitions in that area.

Katz said while the strong pass sales in the Northeast have helped validate the company’s decision to purchase resorts there — in 2019 Vail Resorts acquired Peak Resorts, owner of 17 ski areas in that region — that doesn’t necessarily mean Vail Resorts is looking to acquire more ski areas in the same region.

“I would say that our results to date really confirm that strategy that we’ve had, and our approach to (mergers and acquisitions) remains the same, which is we absolutely are aggressively looking for opportunities in different markets that we think will have value, but we’re going to remain disciplined and only do things that we think will really make a difference,” Katz said.

What would interest Vail in the Northeast? Smugglers’ Notch, adjacent to Vail-owned Stowe, is the most obvious target. Someone will eventually buy Jay Peak, which would instantly join Stowe as Vail’s Northeast crown jewel. Bretton Woods, the largest ski area in New Hampshire, would fit Vail’s portfolio perfectly. And I’ve speculated on possible feeder areas in lower New England that would work well as Epic Pass bases near big population centers. I don’t know for sure, but I do think the company is far from done in the Northeast.

Elsewhere

The Kanc 8 is cruising into place at Loon. Skiing ramps up in Australia and New Zealand. Colorado skier visit numbers came in below the five-year average, while Utah set a new record. Seriously how great was this ski season?

This week in not skiing

A week after I graduated high school I sprained my ankle playing basketball. It swelled to the size of a telephone pole and I couldn’t walk for two months. Which at 18 also meant that I couldn’t work. So all summer I sat on our deck reading Weis and Hickman fantasy novels. I ate Pop-Tarts for breakfast and Jeno’s pizzas for lunch and all day long boats buzzed by on the lake and it seemed no one else was ever at home. In the evening my friends would arrive in their beaten-down 1980s leftover vehicles and they would drive me to Taco Bell and later we’d come back and play poker for hours at the big kitchen table. It is a rich memory despite the absence of duties and it is probably the last time I didn’t have anything to do.

Tomorrow I’m scheduled for surgery to repair a small rotator cuff tear. I don’t even know how the injury happened. I was skiing at Snowbird in December 2019 and at the end of the day my shoulder hurt. I never crashed and there was no trauma. Probably I just overextended dropping into the steeps. I thought it would get better but it never did. For months I had trouble sleeping. A cortisone shot last year seemed to heal things, but an MRI this spring showed the tear getting worse. So even though my life looks vastly different than it did in my post-high school summer, I’m setting up for another stretch of having nothing to do but sit in the heat and read and eat unhealthy food. Of course now I have kids and a mortgage and now I can work from anywhere, injury or no, so I’ll be back to work next week.

But I need to scale back someplace, since I’m going from being able to type probably 100 words per minute to I don’t know maybe eight until my shoulder is mobile. So I’m taking a little break from The Storm. Probably just a couple weeks, but we’ll see. For once I need to not push myself. I’ve got some big things planned for the fall, but hopefully I’ll be back to it before July is out. Thanks as always for reading. I’ll get back to it as soon as I can.

Vail might make play for holiday valley, right now they get 30-40% Ontario residents and blue mountain in ON is a alterra jewel. Vail buying holiday valley could be provide huge Toronto market. Toronto to holiday valley - 3hrs, Toronto to blue - 2.5-3hrs.

reminder that Burke + Jay offer "The Judge" combo pass ....