Independent New England Skiing Welcomes Killington Back to the Fam

“Killington’s future will be guided by the ones that know it best” – Magic Mountain, Vermont President Geoff Hatheway

Perhaps it isn’t exactly accurate to re-classify Killington as an “independent” ski area after its parent company, Park City-based POWDR, announced its pending sale to a group of local investors on Thursday. After all, the ski area is still knitted to neighboring Pico, meaning Killington still technically belongs to a multimountain company (one of 27 such entities based in the United States).

But just everyone is ignoring that technicality, at least for now. POWDR’s sale of Killington shifts the New England ski zeitgeist. Suddenly, consolidation is not the only logical endpoint for large ski areas. Ours is a world where, as in some children’s storybook, magic can still happen. Where, following 40 years headlining conglomerate rosters, the largest ski area in the eastern United States can, improbably and almost fantastically, once again be owned and operated by locals, homeowners and skiers who likely have the means for a fifth home on the side of Aspen Highlands, but have instead thrown in with gritty, chaotic Killington.

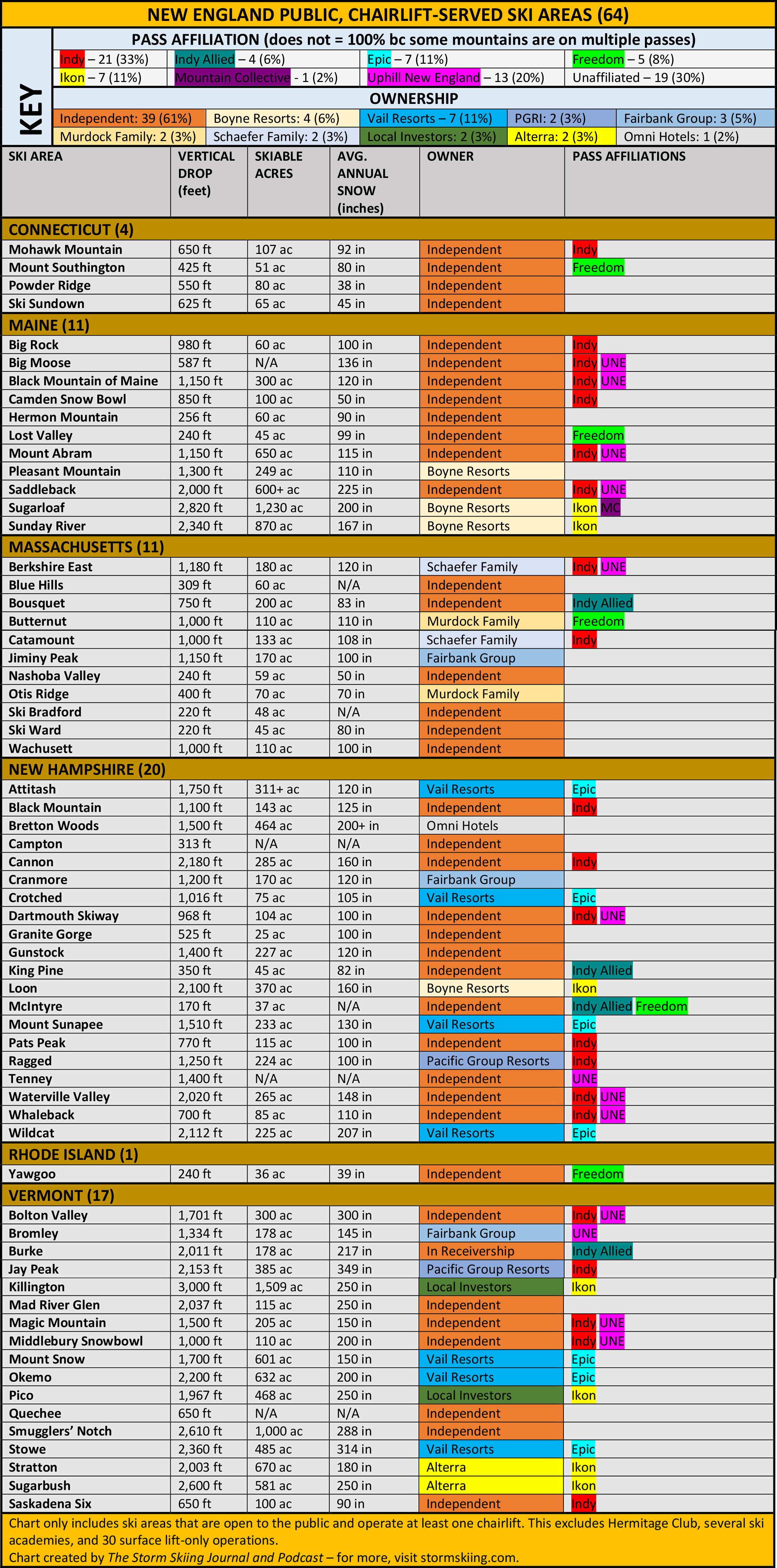

It's easy to overstate conglomerate penetration in New England skiing – 39 of the 64 public New England ski areas with chairlifts are still independently owned and operated. That’s 61 percent of such mountains, and does not include the Hermitage Club and several other private ski areas, or the 30 surface-lift-only operations that dot the region. And just about every operator that does own or manage multiple New England ski areas runs three or fewer, including the Fairbank Group (Jiminy Peak, Bromley, Cranmore); the Schaefer Family (Berkshire East, Catamount); the Murdock Family (Butternut, Otis Ridge); and Omni Hotels (Bretton Woods and a little hill called Homestead in Virginia). Even mighty Alterra, despite the deep penetration of its Ikon Pass, owns just two New England ski areas: Stratton and Sugarbush. Here’s a breakdown of who owns what across the six-state region:

But many of these ski areas are small, remote, and oriented toward a hyper-local audience. Some likely record fewer skier visits in a season than Killington does on a February Saturday. Of the 25 largest New England ski areas, only eight are independently owned and operated (and Cannon and Gunstock are both government-owned, somewhat muting their outlier status), as the chart below shows: