5 Priorities for Alterra’s Next CEO

And 5 things to continue with Ikon and Alterra's owned resorts

The Alterra Mountain Company is a remarkable thing. Its 2017 formation was both elusive and inevitable. Someone was going to have to stand up to Vail Resorts, which over the previous decade had transformed from a regional operator into a national power running 14 ski areas, including four of the five largest in North America, three urban-adjacent Midwest feeders, and, most recently, Stowe, one of the crown jewels of New England skiing. Something was going to have to compete with the Epic Pass, which wrapped all of those amazing places onto one low-cost season pass.

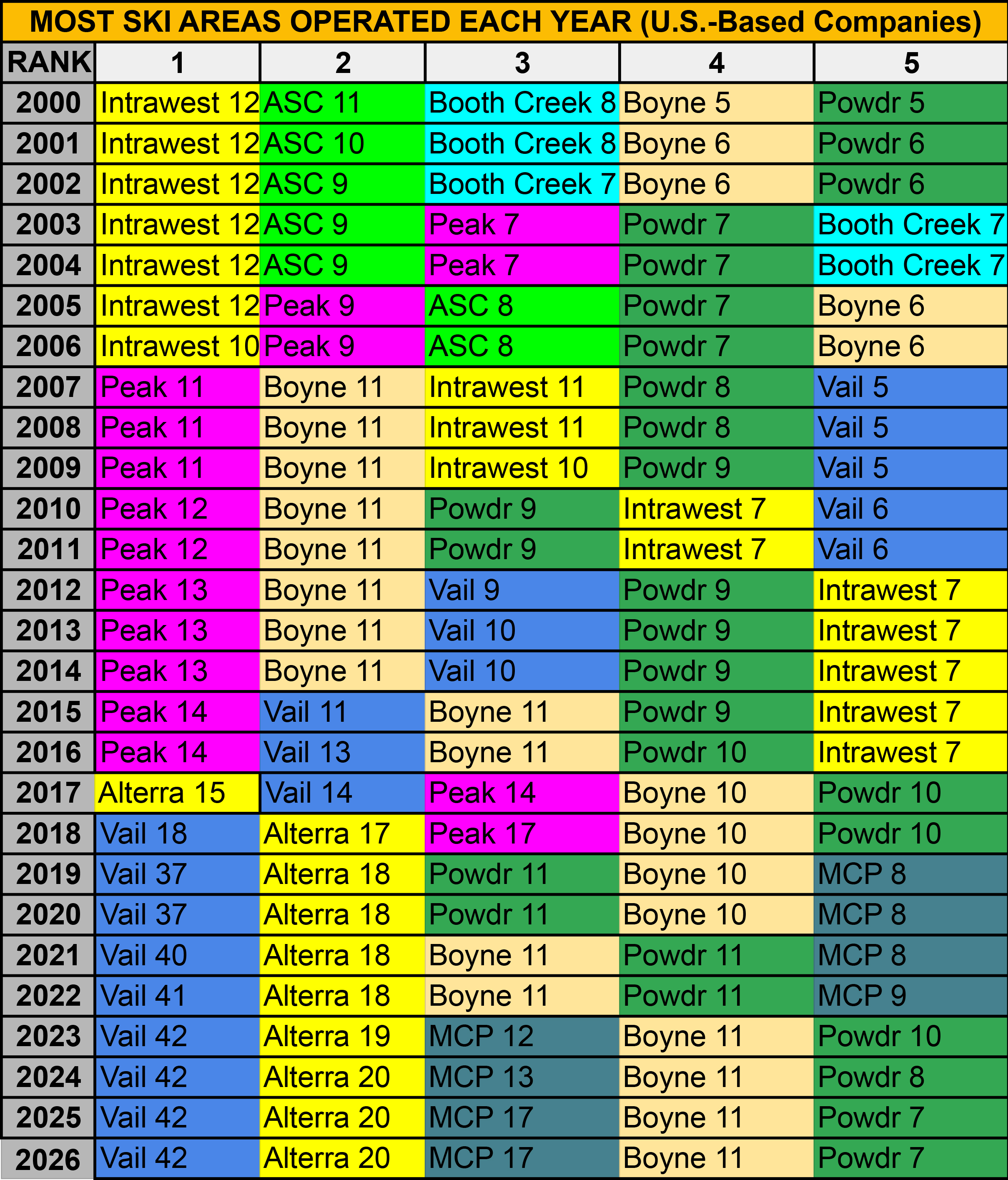

It just wasn’t clear who that someone or something would be. Plenty of operators seemed positioned to challenge Vail’s dominance. Missouri-based Peak Resorts matched Vail in number of ski areas, but it lacked a western anchor resort. Boyne, the quiet, stubborn, family-run survivor, owned 11. Park City-based Powdr, still sore from Vail’s hostile takeover of its hometown resort, ran 10. Once-mighty Intrawest had sold off Whistler, Panorama, Copper, Mammoth, June, and Mountain Creek, but was still hanging around with seven ski areas.

A spirit of cooperation and experimentation prevailed. The previous year, Peak had united its 14 ski areas under the Peak Pass (generating what may be the greatest tagline in the history of ski passes: “How The East Was One”). The year before that, Boyne, Powdr, and Intrawest had launched the M.A.X. Pass, with five days at each of their mountains plus several independents. And nearly two dozen large independent and conglomerate-owned destination resorts had joined the Aspen-sponsored Mountain Collective, which launched in 2012. Copper, Winter Park, and Steamboat had shared a menu of season passes, alternately under shared and competing ownership groups, since the late 1990s.

All good products. All just a little too demographically specific to compete nationally with Vail’s blockbuster Epic Pass, which had sold 650,000 units for the 2016-17 ski season.

Unbeknownst to skiers, nearly everyone not named Vail had huddled in conspiracy. A skiing Manhattan Project, massive and urgent, was underway. In April 2017, the coalition took shape in a motley, yet-to-be-named company sewn from the ghosts of failed and struggling conglomerates past: Intrawest’s seven remaining properties (Steamboat, Winter Park, Stratton, Snowshoe, Silver Creek, Tremblant, Blue in Ontario), re-combined, 11 years after selling them, with Mammoth and June, which had three years earlier acquired Snow Summit and sister property Bear Mountain, which had been grinding through the conglomerate mill for 30 years as is was bought and sold, in turn, by S-K-I (1988), Fibreboard (1995), Booth Creek (1996), and Snow Summit Ski Corp (2002-2014). Funding this union were the twin ski powers Henry Crown and Company (owners of Aspen’s four ski mountains, which would ultimately remain separate), and KSL, owner of Tahoe titans Squaw Valley and Alpine Meadows (the latter had once been owned by Powdr). Six months later, the still-yet-to-be-named entity bought Deer Valley, which had itself three years earlier purchased nearby Solitude. Three months after that, in January 2018, the 14-mountain coalition became Alterra Mountain Company.

Three weeks later, Alterra dropped its atom bomb: the Ikon Pass would join the company’s entire portfolio on one product that would also include access to top destinations operated by Boyne (Big Sky, Sunday River, Sugarloaf) and Powdr (Snowbird, Copper, Killington), along with A-list independents Jackson Hole, Alta, and Aspen-Snowmass. In the leadup to the 2018-19 ski season, Alterra kept buying (Solitude in June; Crystal, Washington in September), and independents (Revelstoke, Sugarbush, Taos), kept joining. In total, Ikon delivered access to 50 ski areas for the 2018-19 ski season at the incredible price of $599 for Ikon Base and $899 for the full Ikon.

Finally, skiing had a true national challenger to Vail, whose Epic Passes were priced that spring at $669 for Epic Local and $899 for full Epic. The consumer response was immediate, total, overwhelming. Snow hammered the West that winter, and exasperated locals raised their pitchforks against Ikon in Jackson, Aspen, and Big Sky. The protests backfired, as the whining only increased Ikon’s visibility and popularity (though Aspen and Jackson would eventually move off Ikon Base and Big Sky would remove tram access from Ikon). Skiers, long challenged to sort through the statistics and logistics of researching, choosing, and accessing remote ski resorts on their own, rapidly understood that they could simply select from one of two destination menus: Epic or Ikon.

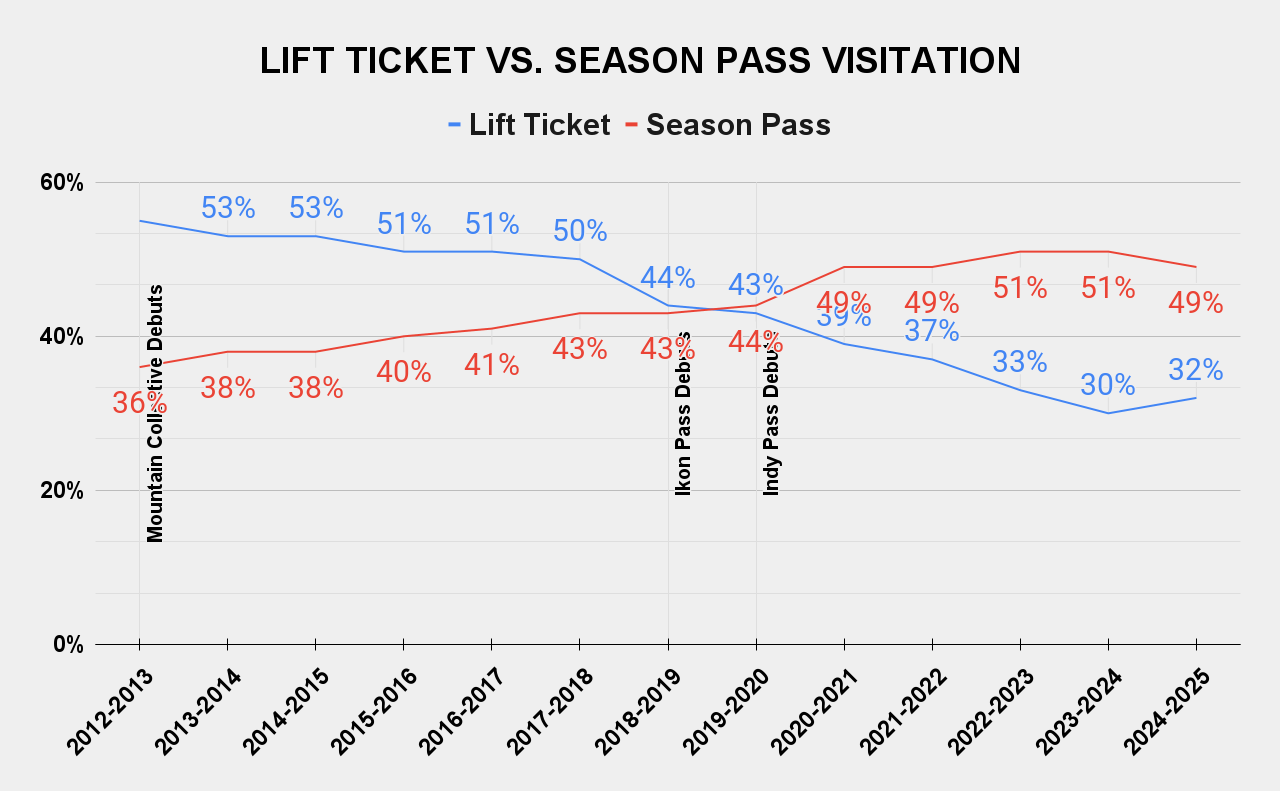

Once that bomb detonated, there was no reassembling it for safe storage. The Ikon Pass altered the lift-served ski landscape instantly and permanently. For ski areas, it normalized the idea that an independent mountain could participate in a larger pass coalition – 242 U.S. ski areas (and 59 percent - 232 of 390 - chairlift-served ski areas), are scheduled to participate in the Epic, Ikon, Indy, or Mountain Collective passes for winter 2026-27. For skiers, Ikon, positioned as a choice against Epic, reset their understanding of what a season pass was and who was allowed to own one, creating a sense of belonging that had been more elusive with a lift ticket dangling from their jacket zipper. The number of skier visits attributed to season pass holders exploded, and within a couple of years had passed the 50 percent mark for the first time.

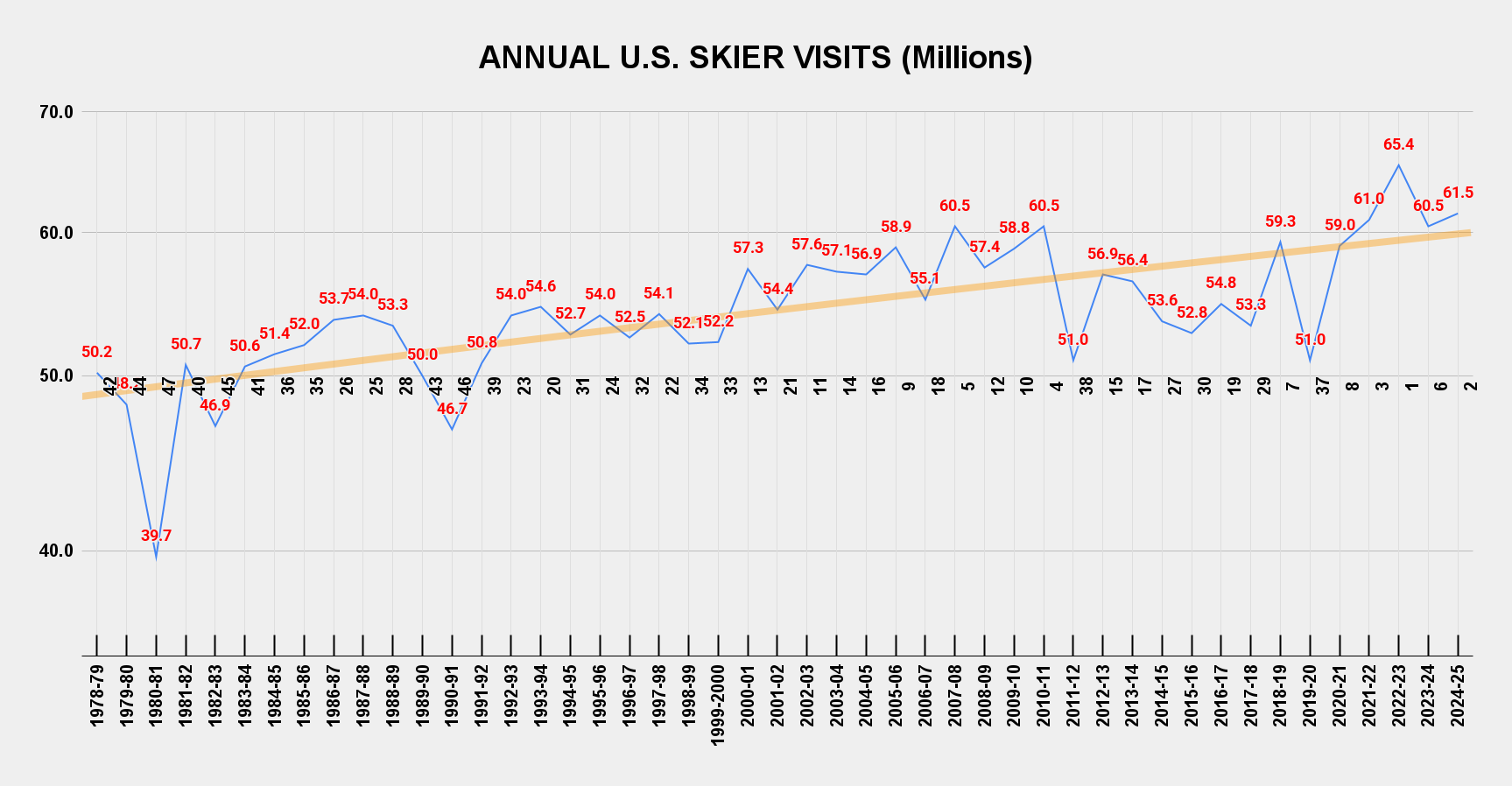

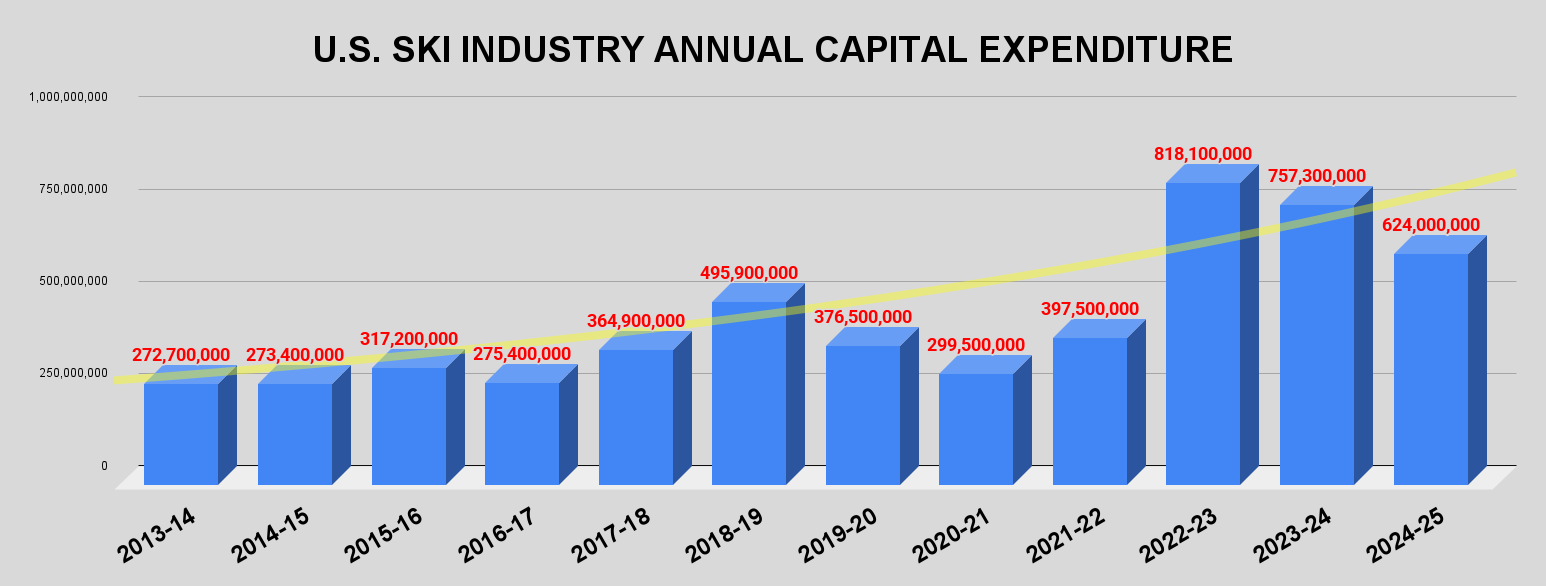

The Ikon Pass was, on the whole, one of skiing’s best ideas. It is probably not a coincidence that American ski areas have recorded top-10 seasons for aggregate skier visits every winter since Ikon’s debut save the truncated 2019-20 campaign, or that capital investment has ramped up enormously since 2018.

It is probably also not a coincidence that consolidation has slowed – and in some cases reversed – as independent ski areas benefit from Epic and Ikon in two ways: affiliation with a national pass product provides a large, reliable revenue stream, reducing the imperative to join a larger company; and skier visit spillover to non-pass-affiliated independents as locals grow frustrated with the tourist patchwork infiltrating the larger mountains.

This all seems so obvious now that it’s hard to appreciate how long this dynamic took to gel, and how recently it formed. There was nothing inevitable about Alterra or Ikon, and there’s nothing inevitable about their continued existence. Vail, after riding the Epic rocket into the stratosphere for 15 years, has struggled post-Covid with shrinking Epic Pass unit sales and skier visits. We don’t have matching figures on privately held Alterra, but the company is in a delicate spot as it seeks a replacement for CEO Jared Smith following an unceremonious ejection last month. A lot of what Alterra is doing has worked really well, but some of it hasn’t, and whoever gets this job next has to take care not to break things that are working as they fix what’s broken.

If I were Alterra’s next CEO, these are five priorities I would start with, as well as five things I wouldn’t dare change: