What Does It Mean When the Snow Doesn’t Come But the Skiers Still Do?

6 potential explanations for a bad winter with good attendance

Omen of doom or reason for optimism in lower skier visit counts?

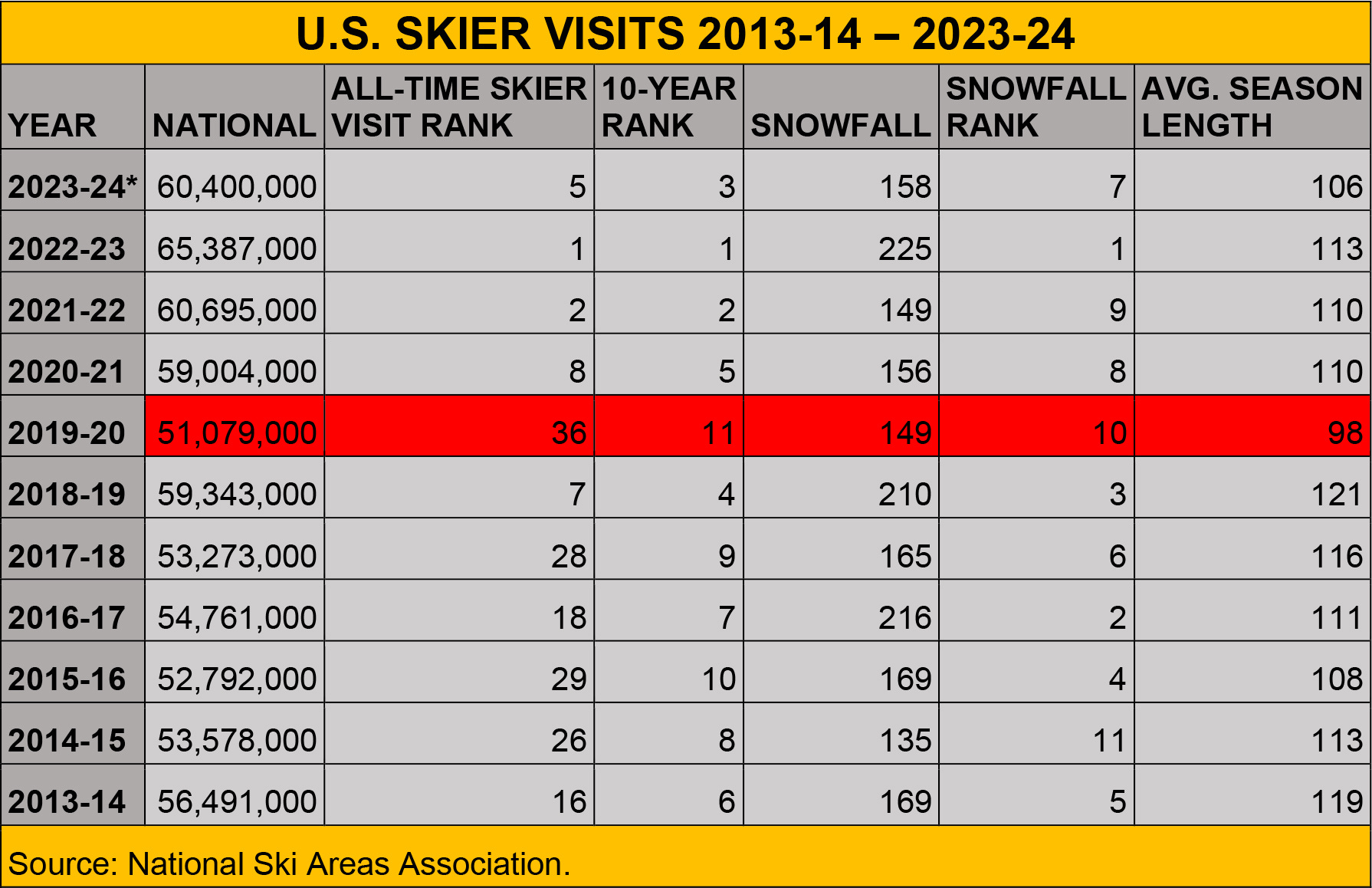

Following two consecutive winters of record-setting attendance, the U.S. ski industry reported a drop in skier visits following the 2023-24 campaign, according to preliminary numbers that the National Ski Areas Association (NSAA) released last month. The total of 60.4 million visits is nearly 5 million fewer than last year’s 65,387,000, a 7.63 percent decline.

These numbers won’t surprise anyone who’s been paying attention. Winter started slow across the continent. By the time the snows showed up, sometime into February, several western ski areas (including Sleeping Giant, Wyoming and Teton Pass, Montana), had cancelled their seasons. Winter barely happened in the Midwest. The big snows came so late to New England that most smaller ski areas had closed for the season by the time storms hit in the latter half of March. The 2023-24 winter ranked seventh in average ski area snowfall over the past 10 winters (tossing out the Covid-shortened 2019-20 campaign), and 10th out of 10 in average season length, at 106 days.

But zoom out just a bit, and it’s actually shocking how not bad skier attendance was this season, given the weather that the pastime depends upon for its very existence. Should these numbers hold (final tallies are due later this year), 2023-24 will stand as the fifth-best season since the NSAA began compiling records, for the 1978-79 ski season. And this winter’s 60.4 million skier visits are less than half a percentage point lower than 2021-22’s at-the-time-record-breaking 60.7 million. Given that last year’s final tally jumped by 700,000 skier visits (from a reported 64.7 million in May to an updated 65.4 million in August), it’s even possible that 2023-24 could finish as the second-best ski season, attendance-wise, in the recorded history of the sport.

How could this be? The Bad Winter = Bad Business calculation has determined the course of recreational skiing since Big Jim Gumshoe towed kids up his Vermont apple orchard behind his trusty mule, Stubborn Stu, for a penny a ride back in nineteen-aught-twelve (the price included a bowl of Martha-Jan’s famous hog’s-feet goulash and a handful of birdshot*). But a number of incremental changes over the past 25 years – only some of them specific to skiing – have, working in tandem, redefined how skiers get on the snow and what happens when they get there. While none of them, individually, really explains how a bad winter can turn into a good winter, they do, considered as a whole, at least help suggest a world in which such a thing is not only possible, but expected. Here are six theories:

1. The “My megapass made me do it” theory

In this world, skiers are skiing more regardless of weather because they’ve already paid for their ski passes. Starting with the introduction of the Epic Pass in 2008, Vail democratized the ski season pass with two fundamental changes: dramatically lowering the price and de-coupling the product from one specific mountain. Not only did Vail Mountain’s season pass price drop nearly $1,300 in one year, but it was suddenly good for unlimited access to four other ski areas (Beaver Creek, Keystone, Breckenridge, Heavenly). And since Vail offered the best price in the spring, wouldn’t sell it at all after early December, and started charging more for a single-day lift ticket than the inflation-adjusted price of the Louisiana Purchase, the Epic Pass quickly gained critical mass.

But not too quickly. Vail sold 204,000 Epic Passes that first season. A decade later – after Vail had purchased Whistler, Park City, and Stowe – the number stood at 740,000. Respectable, but not industry-changing on its own.

Enter: the Ikon Pass in 2018, followed by Vail’s purchase of Northeast giant Peak Resorts in 2019. The multi-mountain pass, once mostly a tool for western travel, suddenly became a standard purchase in the densely populated Northeast. Epic Pass sales have more than tripled in just the last six years, hitting 2.4 million in advance of the 2023-24 winter. While Alterra likely sells fewer Ikon Passes, the two companies have, together, redefined what was once a niche product for locals into a mass-market product for everyone. Even in the Midwest, where Vail and Alterra have little meaningful presence, the percentage of skier visits tied to lift tickets has plummeted from 66 percent over the 2013-14 winter to 52 percent in 2022-23, according to the 2023 Kottke end-of-season survey. For the past five winters, season pass visitation has accounted for more than half of all skier visits.

So now, instead of saying, “it’s snowing, I’ll go buy a $50 lift ticket,” skiers say “well I bought an Epic Pass so I’m going to go to Jack Frost every Tuesday and Stowe for a weekend in January and Park City for a week in March to make sure I get my money’s worth.”

2. The “Gosh counting is hard” theory

In this world, we’re not really seeing more skier visits; rather, as technology for tracking visits has improved and spread, contemporary counts more accurately reflect actual skier visits.