Vail Resorts Adds Seven Springs, Laurel, Hidden Valley Pennsylvania

Acquisition, first under new CEO Kirsten Lynch, gives Vail 40 resorts around the world

Support The Storm by shopping at our partners:

Patagonia | Helly Hansen | Rossignol | Salomon | Utah Skis | Berg’s Ski and Snowboard Shop | Peter Glenn | Kemper Snowboards | Gravity Coalition | Darn Tough | Skier's Peak | Hagan Ski Mountaineering | Moosejaw | Skis.com |The House | Telos Snowboards | Christy Sports | Evo | Hotels Combined | Black Diamond | Eastern Mountain Sports

Vail Resorts on Wednesday announced its intention to purchase Seven Springs and Hidden Valley ski areas in Pennsylvania, and to assume operations of state-owned Laurel Mountain. The $125 million deal would give the Colorado-based company control of eight of the state’s 22 public ski areas and a total portfolio of 40 ski areas in North America and Australia.

The three western Pennsylvania ski areas are jointly owned and managed by Seven Springs Mountain Resort, Inc., part of the business empire of Pittsburgh Pirates owner Robert Nutting. Seven Springs is widely considered one of the top ski resorts in the state and region, and the flagship of the three-mountain portfolio.

The three mountains give Vail a powerful story to tell in the Midwest and Mid-Atlantic, dropping destination-caliber terrain within easy driving distance of its existing Ohio and Pennsylvania ski areas and half a dozen large cities.

“We are incredibly excited to have the opportunity to add Seven Springs to our family of resorts along with Hidden Valley and Laurel Mountain,” said Kirsten Lynch, chief executive officer of Vail Resorts. “As a company, we have been focused on acquiring resorts near major metropolitan areas as we know many skiers and riders build their passion for the sport close to home. These great ski areas in Pennsylvania are a perfect complement to our existing resorts, creating a much stronger connection and compelling offering to our current and future guests in Pittsburgh as well as those in other critical markets such as Washington, D.C., Baltimore and Cleveland.”

This is Vail’s first acquisition since purchasing the 17-mountain Peak Resorts portfolio in July 2019, and the first since new CEO Kirsten Lynch took over for longtime CEO Rob Katz last month. It is also only the second pickup by one of the big four U.S. ski companies since the March 2020 Covid shutdowns (the other was Boyne Resorts’ purchase of Shawnee Peak, Maine in October).

Skiers will not be able to access Seven Springs, Laurel, or Hidden Valley on their Epic Passes until the 2022-23 ski season, and all current reciprocal partnerships will remain in place this winter. Vail has pledged to retain “the vast majority” of each resort’s employees.

Here’s a bit more about what this means for Vail, the Epic Pass, and the ski industry as a whole:

What Vail bought

Seven Springs

Stats: 750-foot vertical drop (2,240-foot base elevation, 2,994-foot summit elevation), 285 acres, 38 runs, 10 lifts, 135 inches average annual snowfall

What we’re working with

My take

This is the prize. If you’re sorting the best ski areas between New England and Colorado, this makes the list. It’s big. The lift fleet is insane: a pair of high-speed six-packs, four quads, four triples. It’s the rare Pennsylvania ski area with marked glades on the trailmap. Everyone loves the place – it consistently finishes in the top 20 on Ski’s annual reader poll of Eastern ski resorts.

It’s not one of the East’s top 20 ski resorts. Those are all in New England. But it is the sort of property Vail covets: busy, built-out, established, and stable. The snowmaking system is outstanding: it was the second ski area to open in Pennsylvania this year (the first was Vail’s Jack Frost), and it will be one of the last to close. The high base elevation helps.

And, like all of these resorts – which sit within 12 miles of one another as the crow flies – it is close enough to big cities to make a viable weekend trip: an hour from Pittsburgh, three hours and change from Cleveland, Baltimore, and Washington, D.C. Combine that with four Vail Ohio ski areas to the west and five Pennsylvania ski areas to the east, and Epic just became the default megapass for every skier from D.C. to the lower Great Lakes.

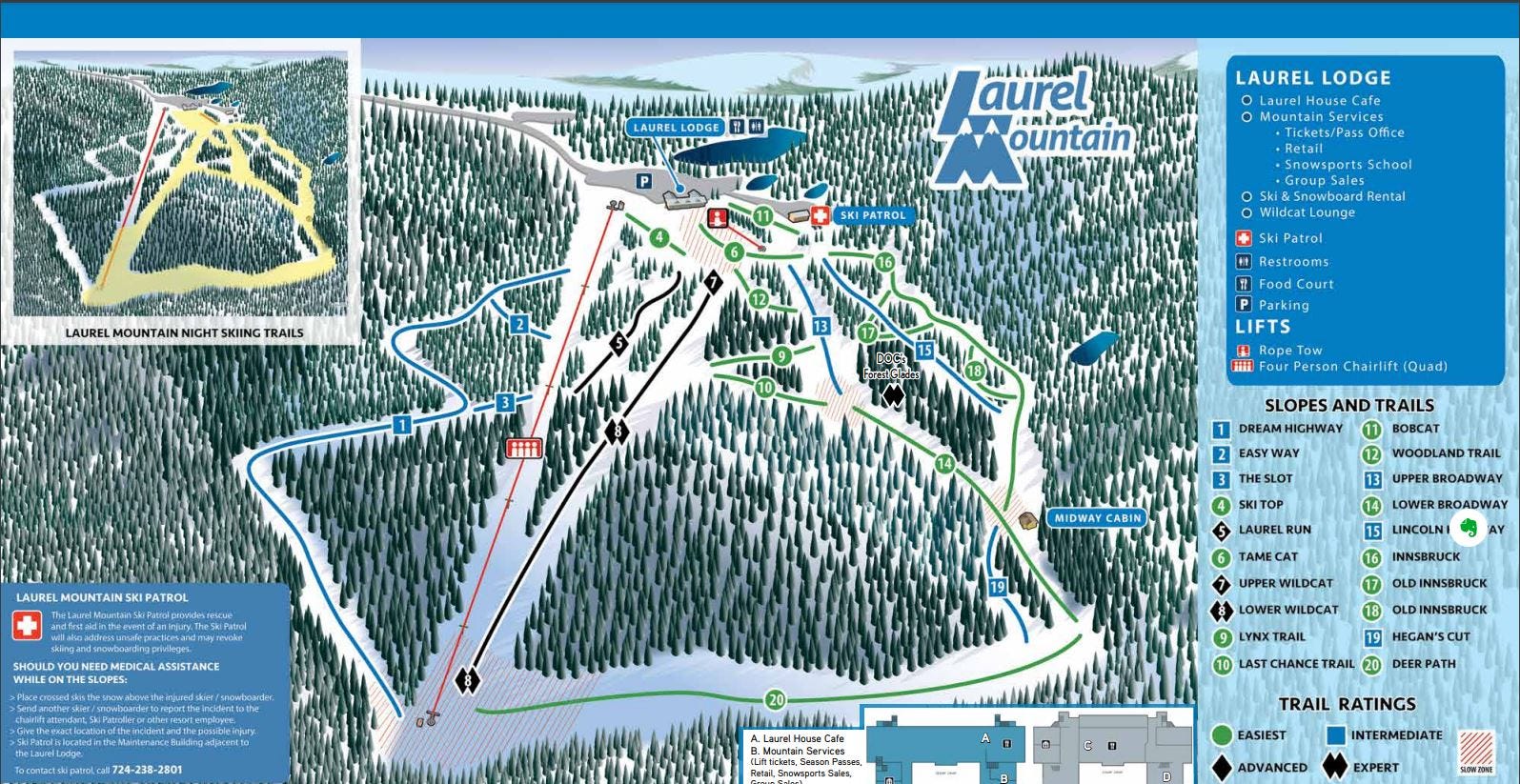

Laurel

Stats: 761-foot vertical drop (2,005-foot base elevation, 2,766-foot summit elevation), 70 skiable acres, 20 runs, 2 lifts

What we’re working with

My take

This place is a miracle, neglected and mismanaged for decades. The ski area’s own website documents its long decline:

In reality, the decade [the 1960s] began the decline of Laurel Mountain. Although the sport saw unprecedented growth in skier attendance and Laurel could still beat Seven Springs attendance 3,300 to 1,200 on a boom Sunday as late as 1965, overall attendance at Laurel declined.

Hidden Valley, Bear Rocks, and Plateau De Mount were new and like Seven Springs, all had easier access from the Pennsylvania Turnpike. The early December opening day 1966 count went to Seven Springs at 3,800 to Laurel’s less than 2,000. Pittsburgh’s newest lift served ski area, Boyce Park (all 180 vertical feet of it), only 15 minutes from downtown Pittsburgh, drew 1600 skiers.

Laurel first chairlift was installed at Laurel Mountain in 1968. A Poma double chair went into operation for the 1968-69 winter and served as it’s only top to bottom lift until 1999.

Despite this long-awaited modern lift the bad news was just beginning at Laurel. Bankruptcy proceedings followed legal fights to terminate the lease and a threatened closure by the state, Patterson won a counter suit and maintained control of Laurel. Amid deteriorating infrastructure, acrimony in the community and new allegations of questionable business practices, Laurel House burned to the ground in January 1971.

Patterson was finally forced out and the state assumed control of operations the following winter.

By the 1971-72 season Laurel Mountain which was Pennsylvania’s most complete and busiest ski area just 10 years prior was reduced to no lodge, no chairlift, two rope tows on the upper mountain, portable johns, no rentals, no snack bar, no running water, and no snowmaking.

Twice the place sat abandoned for a decade: from 1989 to ’99 and from 2005 to ’16. Then Nutting saved the ski area. Laurel is small, steep, and scrappy, with a single five-year-old quad serving the entire mountain.

State-owned Laurel sits within 13,625-acre Laurel Ridge State Park. While massive expansion plans died in previous decades, there is no reason to think Vail could not significantly expand on the property, though I admit I have no familiarity with the local or state politics that may preclude such a project. Vail is currently working through a master plan that would expand its New Hampshire-owned Mount Sunapee, and the company has been managing ski areas on U.S. Forest Service leases since the dawn of its existence. Laurel has enormous potential, and Vail will realize it. And, best of all, give a once-dead ski area an indefinite life.

Hidden Valley

Stats: 470-foot vertical drop (2,405-foot base elevation, 2,875-foot summit elevation), 110 acres, 27 runs, 4 lifts

What we’re working with

My take

Hidden Valley has the kind of layout that makes it ski big: three distinct terrain pods across two peaks. It’s mostly known as a gramps-and-kids kind of place, but it, too, has marked glades. Its lift network is not as spiffy as Seven Springs’ – three of its four chairs date to the 1980s. Vail may change that and it may not – the company has so far not shown much urgency to dispatch outdated lifts at its smaller ski areas, especially if they work just fine. Like Laurel and Seven Springs, Hidden Valley has night skiing.

Which, OK. But let’s move on to the urgent issue here: what is Vail going to do with two Hidden Valleys? The other, in Missouri, sits a mere 10-and-a-half hours by car from its Pennsylvania cousin. The confusion here will be enormous, and my sources in Broomfield tell me this issue is occupying top Vail executives’ every waking hour. They are said to be leaning toward a Hidden Valley Epic Pass, which would give unlimited access to all of Vail’s Hidden Valley ski areas for the 2022-23 ski season.

“But they’re all bowling trophies”

When I was 12 or 13 my friend Chad and I were spending the night at our friend Brad’s house. Once Brad went to sleep in his bedroom, we stayed up in the living room, and in this pre-smartphone era we had nothing to do but notice the things around us. Arranged along a shelf, glittering in the dimlit room, were dozens of trophies.

“You know,” Chad said, “Brad has so many trophies, and he’s so proud of them, but if you look closely, they’re all bowling trophies.”

As Vail pads its portfolio with dozens of resorts, it’s accumulating an awful lot of bowling trophies. Seven Springs is a good acquisition. For Pittsburgh skiers who now have access to Vail’s full menu for less than the price of their Seven Springs season pass, it’s amazing. But outside of investors and regional skiers, this is probably a little ho-hum. No one is cancelling their trip to Whistler to hit Western Pennsylvania skiing.

But this is where we’re at. Vail buys the last half of Pennsylvania. Boyne buys Shawnee Peak. The big stuff has done been bought. There are only so many Super Bowl trophies left: Jackson Hole, Taos, Alta, Telluride, Whitefish. The only big mountain in the country that is actively and publicly for sale is Jay Peak. But expect a lot of these smaller, regionally strategic acquisitions in the years ahead. Personally, I love them, but everyone west of Nebraska has already forgotten about this one.

So what does Vail buy next?

So if Vail’s not buying Sun Valley (which they surely would try to do if it were for sale), then what could they be eyeballing?

We have a few clues. Vail East Region COO Tim Baker told me on the podcast last month that the company was looking for resorts that were “not duplicative,” but complementary to existing properties. As noted above, Seven Springs and its siblings accomplish that, filling what was a 265-mile hole between Whitetail and Brandywine. Vail was also, Baker said, looking for ski areas with rich data mines, presumably to act as proof that these are successful businesses.

Four of Vail’s last five acquisitions were mini-conglomerates that fit all these criteria: Triple Peaks (Okemo, Mount Sunapee, Crested Butte); Australian Alpine Enterprises (Hotham and Falls Creek); Peak Resorts (17 ski areas from Missouri to New Hampshire); and now Seven Springs. All filled holes in Vail’s empire. None was too close to an existing property. And all had strong finances and the data to prove it.

So which existing ski companies fit this description? Certainly two of Vail’s existing Epic Pass partners: Resorts of the Canadian Rockies (Fernie, Kicking Horse, Kimberley, Nakiska, Stoneham, Mont-Sainte Anne) and Sun Valley/Snowbasin. Mountain Capital Partners (Arizona Snowbowl, Brian Head, Nordic Valley, Pajarito, Purgatory, Ski Hesperus, and Sipapu) would fit perfectly, filling Vail’s gaping hole in the Southwest. The jointly owned 49 Degrees North, Washington and Silver Mountain, Idaho could help Vail stamp out a better position in the Northern Rockies. Lutsen, Minnesota and Granite Peak, Wisconsin, would be ideal, and would give Vail true resorts in the region to complement its city-adjacent anthills around Minneapolis and Milwaukee.

There are plenty of one-off properties that would be equally as attractive: Holiday Valley or Bristol in New York; Sugar Mountain, North Carolina; Massanutten, Virginia; Crystal Mountain, Michigan; Whitefish, Montana; Timberline or Mt. Hood Meadows, Oregon. You could think smaller, too, with Seven Oaks, Iowa or Yawgoo, Rhode Island.

Not that any of those are for sale, or will be any time soon. But Vail is clearly looking to anchor itself near any community cold enough to hold snow and attract affluent cityfolk eager to ride the money comet to their Western destinations. And they don’t want fix-up jobs. You won’t find Vail on eBay at 3 a.m. or searching Google Maps for the shell of a ’73 Camaro forgotten in chest-high Alabama side-grass. Vail is shopping at Sotheby’s, looking for the restored antique, the vase pulled from the pharaoh’s tomb, then dusted and polished, ready for display.

Which Epic Pass will these end up on?

Assuming Vail maintains its same basic pass suite, the Epic (starting 2021-22 price $783; ending price $879) and Epic Local ($583-$679) passes will certainly include unlimited access to Seven Springs, Laurel, and Hidden Valley. Interestingly, the Northeast Value Pass and Northeast Midweek Pass included not only Vail’s properties in New England, New York, and Pennsylvania, but also Ohio and Michigan. Should this geographic footprint remain intact, the three western Pennsylvania ski areas would join them. And good God what a bargain: the Northeast Value Pass started at $479 this year and topped out at $511. None of Vail’s five other Pennsylvania ski areas came with any blackouts on this pass, and there’s no reason to suspect the new ones would either. The Northeast Midweek Pass – starting at $359 and going off sale at $383 – had a few holiday blackouts.

Compare those prices to Seven Springs’ Highlands Pass, which delivers unlimited access to all three ski areas and started at $643 in the spring. The final price landed at $675. So for less than the price of that three-mountain pass, Seven Springs skiers who pick up a Northeast Value Pass will now get access to Stowe (10 days), Wildcat (unlimited), Mount Snow (limited blackouts), and much more. For $80 less than the early-bird price, they can get an Epic Local Pass, and hello Whistler, Tahoe, Vail, Summit County, Park City. The value and access here is tough to comprehend, especially when you bring the single-mountain season passes at Laurel ($483-$507) and Hidden Valley ($497-$522) into the conversation.

With such an enormous footprint in Pennsylvania, Vail does have an opportunity to establish some kind of Pennsylvania pass. Historically, they have been pretty inventive with regional Epic Passes, with versions for Colorado’s Summit County and their Lake Tahoe resorts. Vail even offers a little-known Ohio Pass, which grants unlimited access to their four ski areas there for around $300. Could we see a Midwest-Mid-Atlantic pass? Maybe. But the Northeast Epic is already a steal. I’m not sure how much lower Vail could realistically go (or why they would need to drop the price when Seven Springs skiers are getting so much more for less than what they’ve historically paid).

Is this skiing’s version of Standard Oil?

A long time ago, around the time the internet was really catching on, Vail tried to buy three ski resorts that were spaced not much farther apart than this western Pennsylvania trio. The Justice Department said “no.” The reasoning was that “the deal likely would have resulted in higher prices to skiers…” So Vail got Keystone and Breckenridge, and neighboring Arapahoe Basin remains independent to this day.

How quaint. Does anyone doubt that the Justice Department’s only response to the same deal today would be, “well at least Bezos isn’t buying it?” We’ve been watching mega-industries like banks and airlines consolidate for years, under Republican and Democratic administrations. And while occasional deals get shut down, most don’t.

Which is not the same thing as saying that this deal should go through. Should Vail own eight of 22 public ski areas in a single state? Probably not. I don’t have concerns about price – the company seems determined to keep skiing accessible to the masses. But these passes are so good that it is easy to see them cannibalizing business from weaker competitors. The Poconos ski areas – adjacent to Vail’s Jack Frost and Big Boulder – should be fine. But I worry about places like Blue Knob, an extra hour east of Laurel from Pittsburgh. The place is an Indy Pass partner with an 1,100-foot vertical drop and a killer trail network. It’s also an absolute disaster, underinvested in snowmaking, unable to maintain consistent operations in any but the best years. How does this place, with its low-rent website and top-of-the-mountain access road, draw enough skiers to make the necessary capital investments when Vail is tossing Epic Passes out the window like the mayor with a bagful of Tootsie Rolls at the Founder’s Day Parade?

You can save your email, Free Market Bro. It doesn’t matter what I say or what anyone says – this deal will happen.

So Alterra just let me know when you schedule the hostile takeover of Camelback

I still can’t figure out why Alterra parent KSL Capital purchased Camelback and Blue Mountain and put them under the Krusty-the-Clown leadership of KSL Resorts, rather than Alterra, home to some of the best ski resort operators in the world. I wouldn’t put the knuckleheads at KSL Resorts in charge a vacuum cleaner, let alone a ski resort. While they’ve taken control of Blue Mountain too recently to ignite any sort of major catastrophe, their short tenure at Camelback has featured a loaded chair falling off a chairlift, a young girl detaching from a zipline, and an employee getting run over by a Snowcat. Good job.

Alterra, you need Ikon Pass representation in Pennsylvania yesterday. You now have Snowshoe competing against 12 ski areas from Cleveland to Philly. Send the buffoons at KSL resorts back to run their 19-star beachside oases in Cabo San Positano so we can get Camelback and Blue on the Ikon Pass.

But then the Ikon Pass would have two Blue Mountains. Damn it! There’s got to be a better way, America!

One quick note on your otherwise fantastic summary of this transaction and its ramifications. When Vail talks about targeting "data rich" ski areas for expansion, it's almost certainly not a reference to the detail they can provide on their financial statements supporting the historical cash flow/acquisition price - that's table stakes. Rather, it's customer data from their CRM system that Vail can ingest into their central platform and then sell/market the hell out of the Epic Pass and related offerings. You could acquire the biggest, baddest ski resort in the world, but if you don't have data on your customers, then Vail isn't going to be interested b/c the value prop is all in the cross-sell.

I think Boyne would be a good fit for Blue Knob. With some investment, Blue Knob could be a Brighton of the east. Same rustic feel, great terrain, and a mountain that skis bigger than it is. Plenty of room to expand too.

They could probably pick it up cheap and start with snowmaking. Replace the lodge and then upgrade the lifts.

Put it on a Boyne or Ikon pass and they have a feeder resort to New England and the West.