The Western U.S. Has Added 54,598 Acres of Skiable Terrain Since 1994

That’s like adding another Colorado (and then some)

If ski “supply” is “flat to shrinking,” then how did we add another Colorado’s worth of terrain since 1994?

Let me say off the top that I like, respect, and use Motley Fool’s investment advice. This is not an attempt to flame them or Brobot call-out a #FakeSkier. But I groaned when I read this snippet in a recent Fool article ($) analyzing Vail Resorts stock (ticker: MTN):

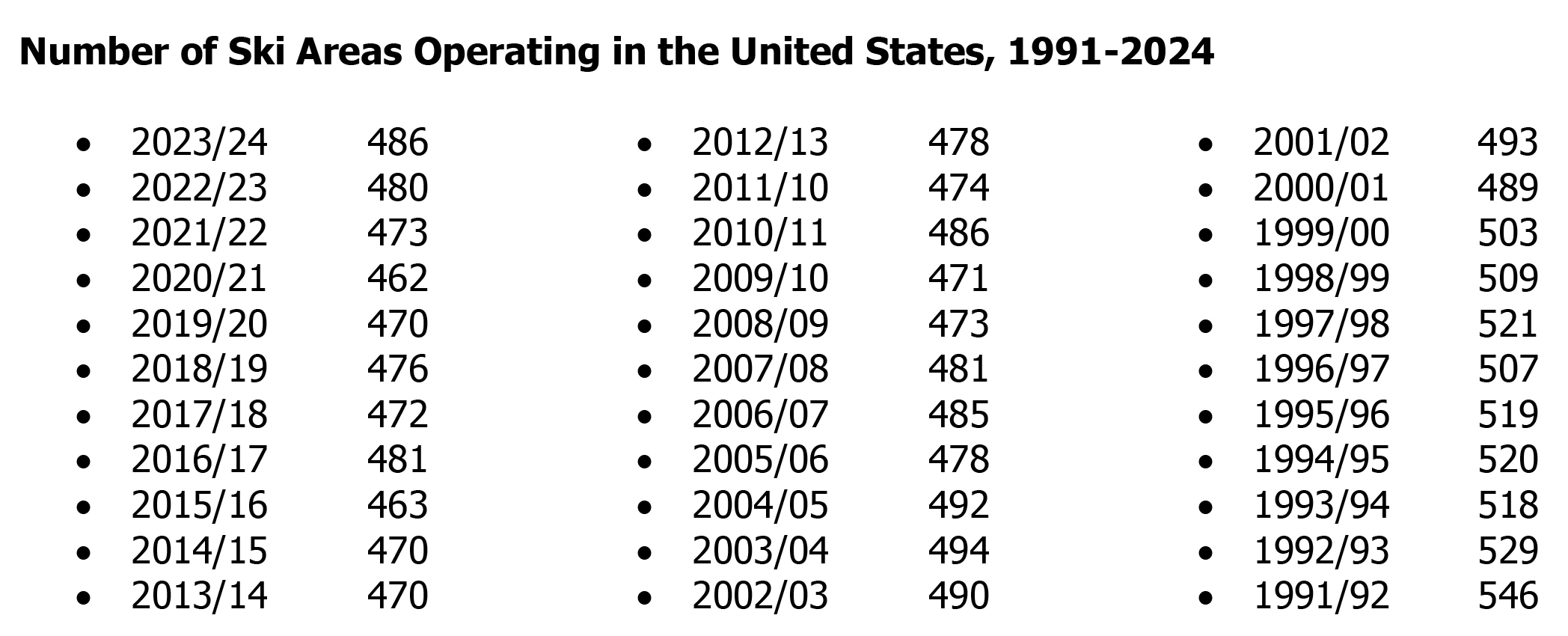

During the 1992 ski season, there were 546 ski areas operating in the United States compared to about 486 today. Supply is flat to shrinking. On the demand side, 3 of the top 5 busiest ski seasons on record occurred each of the last three years. Demand is up. Furthermore, a key revenue driver for Vail, the EPIC Pass, is nearly $400 cheaper than the rival IKON Pass despite providing access to more ski resorts. That should give Vail considerable pricing power for years to come, including its 7% price hike to the EPIC Pass for the 2025-2026 ski season.

Some of this is just wrong:

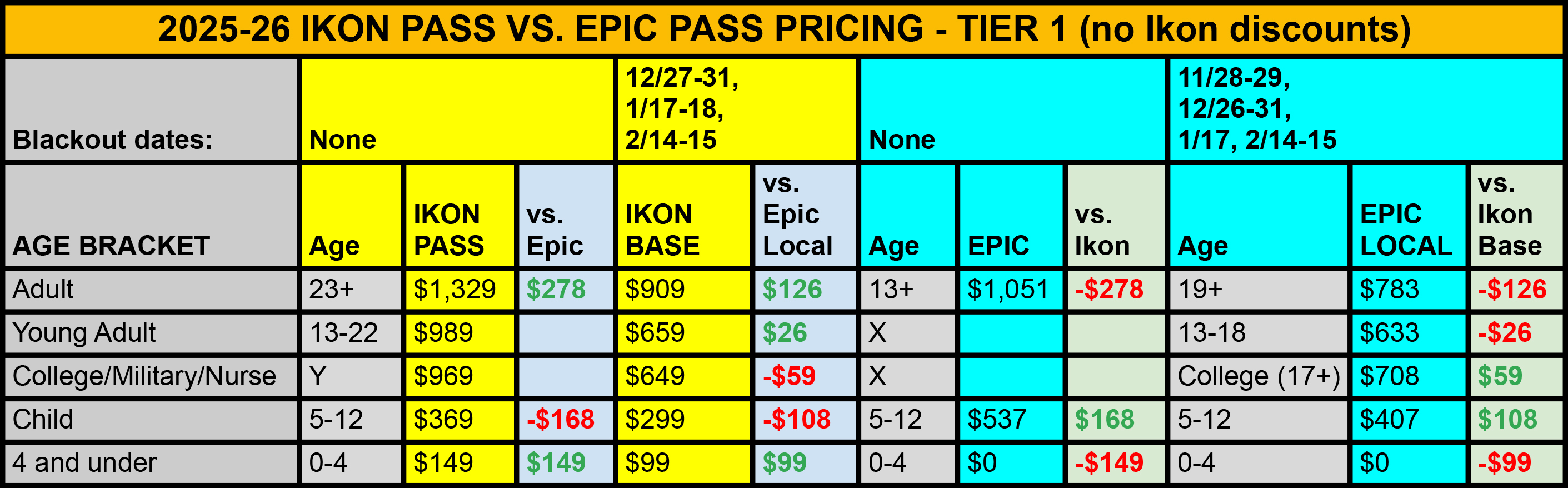

Skiers will be able to access 75 ski areas on their 2025-26 Ikon Passes, compared to 65 on Epic (I’m counting individual ski areas, not Ikon’s “destinations,” which often group several ski areas, lumping, for example, the four Aspen mountains into one).

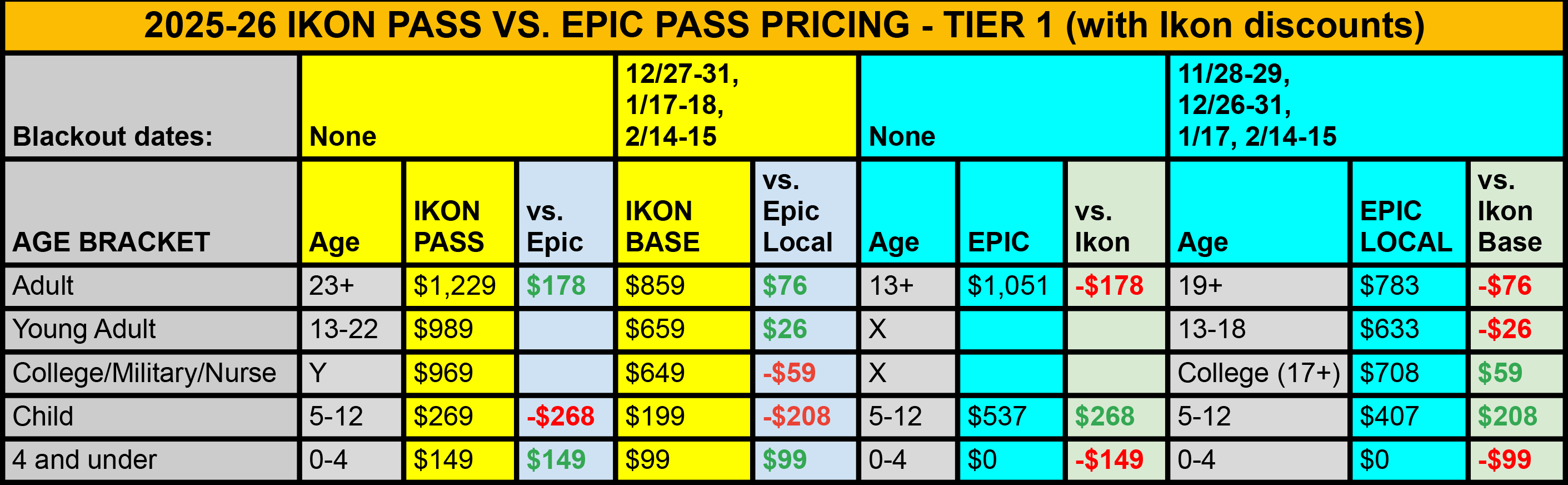

Epic retails for $1,051, just $278 more than the $1,329 Ikon Pass; Ikon’s renewal discount drops that to $1,229 – a $178 premium to Epic. I’m no finance genius, but neither of those price differentials count as “nearly $400” around these parts.

Pricing nuances abound between the two product suites – Ikon’s child passes are much cheaper than Epic’s, and are discounted with the purchase of an adult pass; the difference between Ikon Base and Epic Local is also quite small. Chartage:

And here’s the difference across the main Epkon product suites if you consider Ikon renewal and child pass discounts:

But those are minor issues, easily untangled by anyone with an internet connection and a calculator. The real problem with the above paragraph is the first two sentences, pointing to the shrinking number of U.S. ski areas as evidence that the “supply” of lift-served skiing is declining.

Right about now, you’re saying, “Bro, the numbers!” And I’m saying, “Bro, I know. Just hang on.” I know where these numbers come from: the National Ski Areas Association’s fact sheets:

And what could possibly be a better source than the trade association that represents the American ski industry, right?

Right. I agree. The raw numbers of ski areas are accurate enough (though I keep a separate list and count 505 active ski areas for the 2024-25 ski season, nine more than the 496 I counted last year, which was 10 more than the NSAA’s 2023-24 count of 486; we’ll deal with that discrepancy in a future column). But let’s just say that approximately 10 percent fewer ski areas are operating in America this winter than in 1992. That’s bad, right?

No. And here’s why: while the raw number of operating ski areas declined rapidly through the 1980s and ‘90s, that number stabilized around 2000, and the skiable acreage at the surviving U.S. ski areas is, cumulatively, far larger than it was in 1992.

How much larger? I haven’t calculated exact figures (a likely impossible task), nor have I examined the entire nation. But I did compare and total the current skiable footprint in the 11 contiguous western ski states (Colorado, Utah, Arizona, New Mexico, Nevada, California, Oregon, Washington, Idaho, Wyoming, Montana) to their listed acreage in 1994’s Peak Ski Guide & Travel Planner, which billed itself as “the official ski areas guide of U.S. skiing.” In that analogue era (the guide’s 440 pages don’t list a single website, not even in the ads), many ski areas did not advertise a skiable acreage total. I set those facilities aside (I’ll address them down the post), and tallied up the 92 mountains that Peak listed a skiable footprint for and that are still in operation today.

Here's what I found: those 92 ski areas have grown by a combined 52,083 acres since 1994. Acres are difficult to visualize, but check out this itemization of current skiable acreage by state:

Colorado, king of U.S. skiing, responsible for approximately one in four skier visits in an average ski season, offers 45,552 acres of skiable terrain for the 2024-25 ski season. That means that the United States has added the equivalent of another Colorado to its skiable footprint since 1994.

“Bro why are you writing in italics so much today? ARE YOU GOING TO START WRITING IN ALL CAPS WITH BOLDFACE AND QUESTIONABLE UNNECESSARY PUNCTUATION NEXT??!??”

You’re right, Grammar-and-Style Bro, I am pushing it. But I really need to make this point, because non-ski media reaching for Death-of-Skiing narratives are going to continue pointing to the raw ski-areas-in-existence stats and declaring, with no context or additional evidence, that CLIMATE CHANGE IS KILLING SKIING!!!

The actual narrative is more complex: most of the ski areas that have failed since 1992 were small and mismanaged (climate change hasn’t helped, but snowmaking works). The ski areas that survived did so in part because they funneled their profits into expansions and snowmaking. The result is fewer, but healthier, businesses serving more skiers in a more streamlined fashion than they could have done in the mostly-fixed-grip lift, energy-intensive-and-inefficient snowmaking, wicket-tickets-and-lines-for-everything cash-economy no-internet early 1990s.

To underscore the point that ski “supply” is expanding, not shrinking: the 52,083 acres cited above leaves out 76 western ski areas that presently total 39,069 acres. Most existed in 1994, but Peak did not provide a contemporary acreage stat. Six of these 76 ski areas have came online since, including 1,819-acre Silverton, opened in 2001; 1,100-acre Tamarack in 2004; 1,000-acre Blacktail in 1998; and 400-acre Cherry Peak in 2015. Those four ski areas’ 4,319 acres more than offset the combined 1,804 acres lost when the 10 ski areas that Peak listed as active in 1994 ceased operations. Here’s how that all sorts out:

To add all that up: 52,083 acres of new terrain at existing mountains PLUS 4,319 acres at new public ski areas MINUS 1,804 acres worth of lost ski areas EQUALS 54,598 acres of new ski terrain in 11 western ski states since 1992.

Here’s a deeper look at how I compiled this data, why the total of new acreage is likely even higher, where ski area growth has been concentrated over the past three-plus decades, and the ski areas that have failed. Lots of chartage, Brah:

The chart, with asterisks

Here’s an itemization of those 92 western ski areas, listed in order of their current skiable acreage footprint:

Yes, there are a lot of asterisks in there (well actually there are no asterisks because they anger the robots, but I trust in the power of your imagination):

I intentionally left off Mountain High and Big Bear. Both listed odd, larger-than-their-present-footprint combined acreages across their multiple ski areas - which were then and now physically separate – in the Peak guide. I don’t know if this was the result of some weird 1990s marketing war or just changing standards of measurement. Both complexes together total fewer than 1,000 acres, and both are still fully operational (with the exception of tiny Mountain High North), so they are not statistically significant here.

I immediately violated any standard that the first bullet set by including Sun Valley, which then and now lists combined acreages for Bald and Dollar Mountains, despite the fact that they are separate ski areas with no ski or lift connection. But the whole complex only grew 54 acres over the past 31 years, so it didn’t really mess anything up.

The 1994 skiable acreage listed for Park City – 3,050 acres – includes 2,200 acres for what was then Park City Mountain Resort and 850 acres for next-door-neighbor Wolf Mountain, which later became Canyons, which in 2015 became part of Park City when Vail Resorts built a gondola connecting the two.

The 1994 skiable acreage for Palisades Tahoe includes 2,000 acres listed for Squaw Valley and 2,000 acres for Alpine Meadows (actually, the guide lists 10 acres for Squaw and 2,000 for Granlibakken, which are right beside one another in Peak’s chart; given that the two are just a few miles apart, I am assuming this was a missed copy-edit). Alterra, of course, combined the ski areas via gondola in 2022 after changing the name of the entire complex in 2021.

The 1994 skiable acreage for Beaver Creek includes Arrowhead, which the larger ski area absorbed in 1997.

Cuchara, Colorado appears to have shed 300 skiable acres, but there’s an explanation: the ski area’s 330 acres on four chairlifts sat dormant for two decades, until a local group launched a revival a few years back. They shuttle skiers to the top of Chair 4 (the shortest one), while they work to restore the lift. Skiers can skin the rest, 1,562 vertical feet.

I don’t know what to make of the other three ski areas that report smaller skiable footprints in 2025 than they did in 1994: Howelsen Hill, Elko Snowbowl, and Kelly Canyon. None, as far as I can tell, have suffered from any sort of terrain contraction. It’s a total of 160 acres, however, so I’m just going to shrug and keep moving.

A handful of ski areas went under different names in 1994: Whitefish was “Big Mountain”; Discovery was “Discovery Basin”; China Peak was “Sierra Summit”; Eagle Point was “Elk Meadows”; and Buttermilk was “Tiehack” – these, and the Palisades/Park City/Beaver Creek roll-ups itemized above, are the sorts of things that non-ski media point to and say, “See, these ski areas just DISAPPEARED.”

What Peak left off

The 1994 Peak guide listed skiable acreage totals for most, but not all, western U.S. ski areas of 1,000 acres or more. Check out some of the monsters it left off (the ones highlighted in yellow have been built since 1994):

Excuse me while I dodge the tomatoes that you’re chucking at me for including Wasatch Peaks Ranch and Yellowstone Club on this list. So let’s subtract their combined 5,700 acres from the 39,069-acre total – that still gives us 33,369 acres of terrain that Peak didn’t account for in 1994. But while we can’t compare the exact combined acreage of these ski areas from then to today, we don’t need to dig too deep to establish that their overall footprint has grown substantially over the past 31 years. Consider:

Silverton, Tamarack, Blacktail, and Cherry Peak together added 4,319 acres of skiable terrain to whatever the 1994 total was

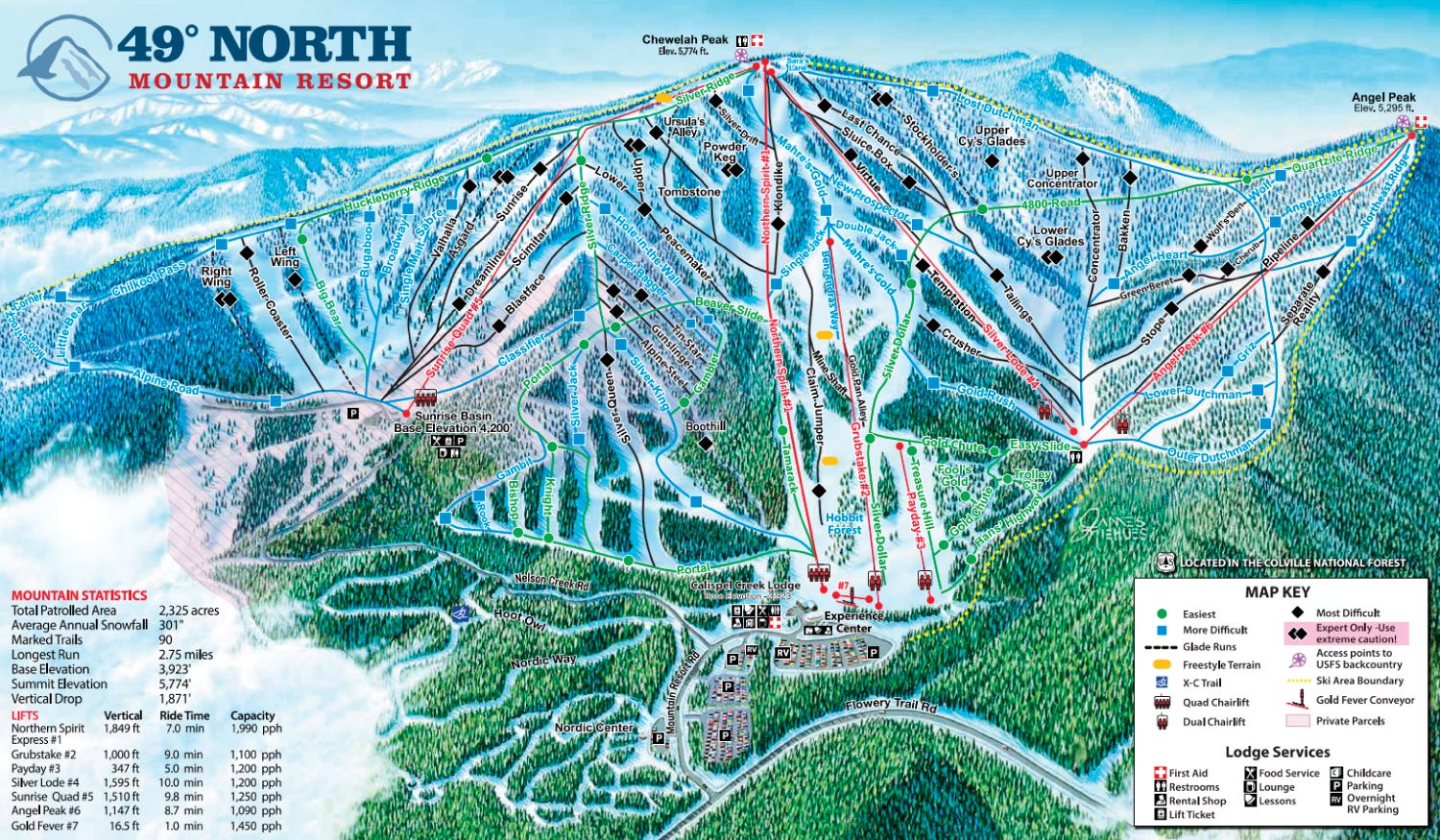

49 Degrees North ran four chairlifts on a small footprint in 1992, and has expanded east and west in at least three major phases since. Conservatively, it has probably tripled in size:

Other significant expansions among this group include Northwood at Mt. Spokane (2018); Wild West at Great Divide (2001); and Timberwolf (2003), Northstar (2007), and Eagle Peak (2022) at Lookout Pass.

So let’s say, conservatively, that the West has added another 8,000 to 10,000 acres of public skiable terrain since 1994 between expansions and new ski areas, in addition to the 52,083 quantifiable-by-comparison acres listed in the 1994-to-2025 comparison chart. If we call it 60,000 acres, that would give us the rough equivalent of another Colorado (45,582 acres of skiable terrain) and another Washington State (15,662 acres).

What I left out

For now, the West is sufficient to demonstrate my point that ski “supply” is expanding, but at some point, I will likely add the 1994 totals for the remainder of the U.S. ski states. I skipped this step for now, as this exercise is unlikely to uncover more than a few thousand new acres of skiable terrain, despite the abundance of ski areas throughout the Midwest and East. Why? Here are current skiable acres by state:

That’s because ski areas in the rest of the country are so small, right? Not exactly. One of the great regional differences is that western ski areas tend to count everything within their boundaries as skiable terrain, while ski areas elsewhere typically just count trail acreage (Killington and Smugglers’ Notch are exceptions in the East). There’s some logic there, as the West’s more reliable snowpack opens most of the terrain on most of the region’s mountains most of the time. And with less-dense tree cover, that terrain is easier to get into, in general. But it snows in the East, too, and some little mountains feel 10 times larger once the snow settles. Plattekill, New York, for example, only lists 119 acres, but thanks to summer glade-thinning parties, nearly all the trees are skiable, making powder days feel huge.

Another reason to eventually itemize the eastern ski areas is to address another potentially alarming statistic: five states that once hosted lift-served ski areas no longer do. That’s 10 percent of the states! But those states are Georgia, Kentucky, Kansas, Arkansas, and Nebraska. What happened to them is a subject worth addressing, but it was a small number of small ski areas – most of which were long gone by 1994 – so it can wait.

What if the ski areas just inflated their acreage totals in some decades-long marketing war?

This is a fair question. And, indeed, the skiable footprints of Palisades Tahoe’s legacy ski areas appear to be substantively the same as they were in 1994. But the expansions of Park City, Big Sky, Vail Mountain, Powder Mountain, Bachelor, Steamboat, Northstar, Keystone, Winter Park, Snowbasin, Breckenridge, Targhee, Copper, and just about every other ski area on this list are enough to explain their individual acreage increases. See the growth for yourself by browsing the past three decades of trailmaps.

OK but what about those lost ski areas?

Yes, we’ve lost some ski areas since 1994, some of them quite large. Here’s a list of the 10 lost ski areas that the Peak guide listed as active across our 11 contiguous western ski states in 1994. I also added two sporadic operators that may have opened that winter, but that the guide elected not to include, likely because they were already mid-failure: Iron Mountain, California and Berthoud Pass, Colorado:

But there are nuances to this list. Breaking it down:

The only sort-of lost

Most of these ski areas have not operated as lift-served enterprises for years, but some “well-maybe” storyline is attached to each of them:

Elk Ridge is owned by Mountain Capital Partners, the same outfit that owns nearby Arizona Snowbowl. They’ve confirmed to me many times that they would like to get the ski area open again, but are sorting through permitting issues.

Mt. Waterman operated last year (albeit for the first time since 2020). The new owner has some wacky idea to turn the bump into a private club that rich people fly to in their helicopters. It is right above Los Angeles, so maybe. But the thing Waterman really needs is snowmaking and an agreement with Caltrans to plow the road up to the resort after snowstorms.

A local group has transformed Marshall into a public park. They removed the lift recently, but you can backcountry ski there all you want.

Spout Springs dropped dead around 2017, but the Forest Service has been actively searching for a new operator. The lifts are all still intact, though one of them looks like it walked into the wrong bar on beat-up-the-chairlift night.

I don’t really know what’s going on with Kratka Ridge or Green Valley, but the Forest Service still lists their leases as active – meaning someone could reactivate the ski areas if they had the money/patience/aptitude to do so. I hiked Kratka Ridge a few summers ago, and was stunned to find an intact single-person chairlift climbing the steep hill:

The probably-doesn’t-matter-much-that-it-was-lost

Yes, I know #AllSkiAreasMatter, but these bumps likely faded before we figured out that the only way to keep surface-lifts-and-two-runs ski areas operating is by installing a snow-tubing operation right next door.

Hitt Mountain is so obscure that even the internet hasn’t heard of it. The Peak guide listed no stats, and none of my other vintage guidebooks mention the place.

Snowshoe Hollow is similarly lost in time. One ropetow and two runs probably did not open a new fault line at collapse.

The lost-and-that-just-plain-sucks-because-these-places-would-have-come-in-handy-in-the-Epkon-era

And sometimes we lose ski areas that really meant something, and they’re probably gone forever (though perhaps I’m burying Ski Rio too soon):

North South Ski Bowl was the only game in its neighborhood. This is the sort of just-big-enough learning center that minted kids who would pinwheel off into the Rockies as improbable but fabulous skiers.

Berthoud Pass is exactly the sort of ski area that jammed-up and beaten-down Colorado needs right now: simple, close enough, big enough. You pass it on your way up to Winter Park. The chairlifts are long gone, as are the permits to operate a ski area on the site.

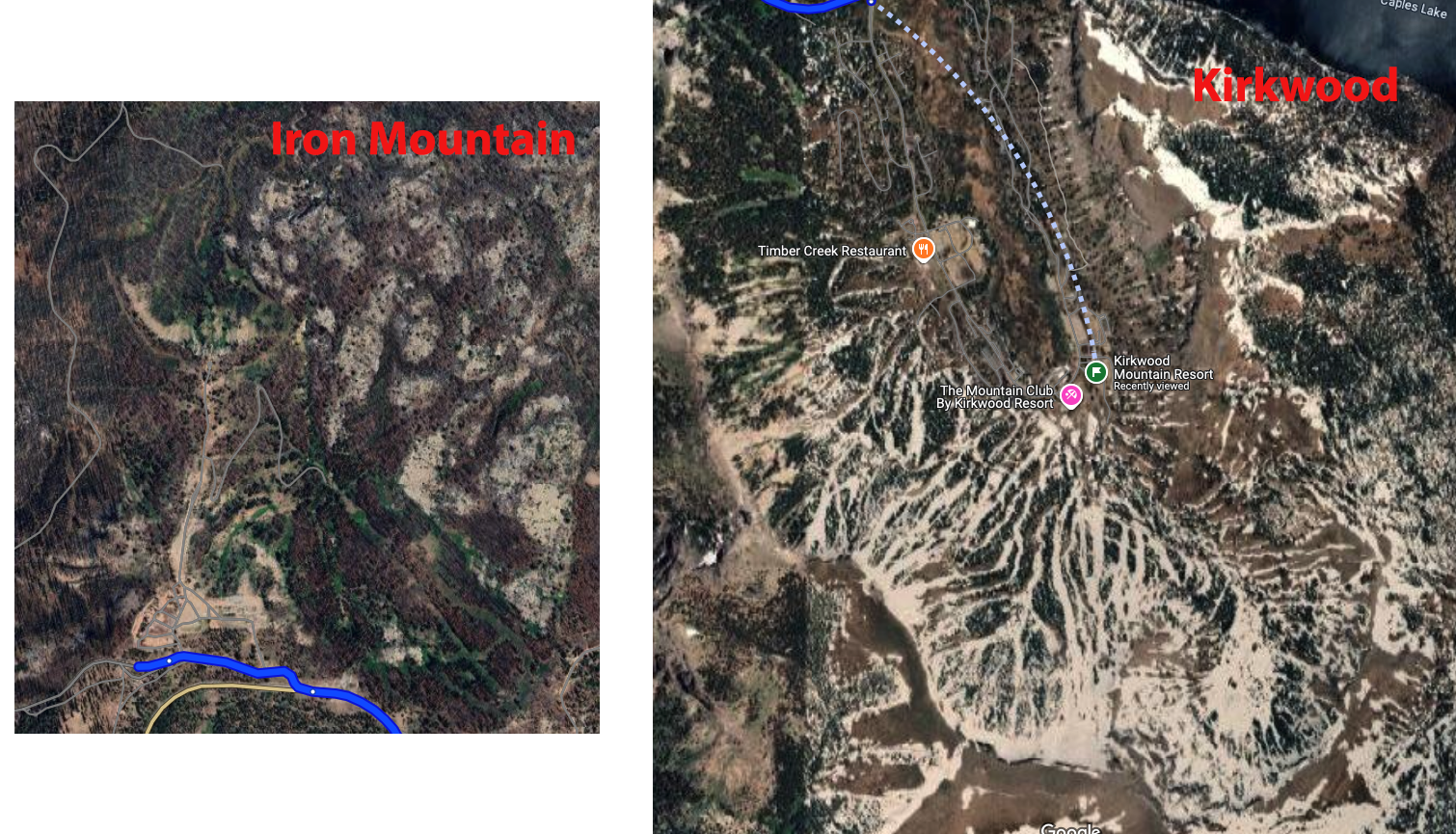

Iron Mountain is a weird one. Weird that it failed, I mean. It’s right down the street from Kirkwood. Tahoe and California can clearly support a lot of ski areas. This one is listed in a few places as 1,700 acres, which would make it nearly the size of Kirkwood and Sierra-at-Tahoe. I’m not buying that, because look at the trail footprints side-by-side on the same scale:

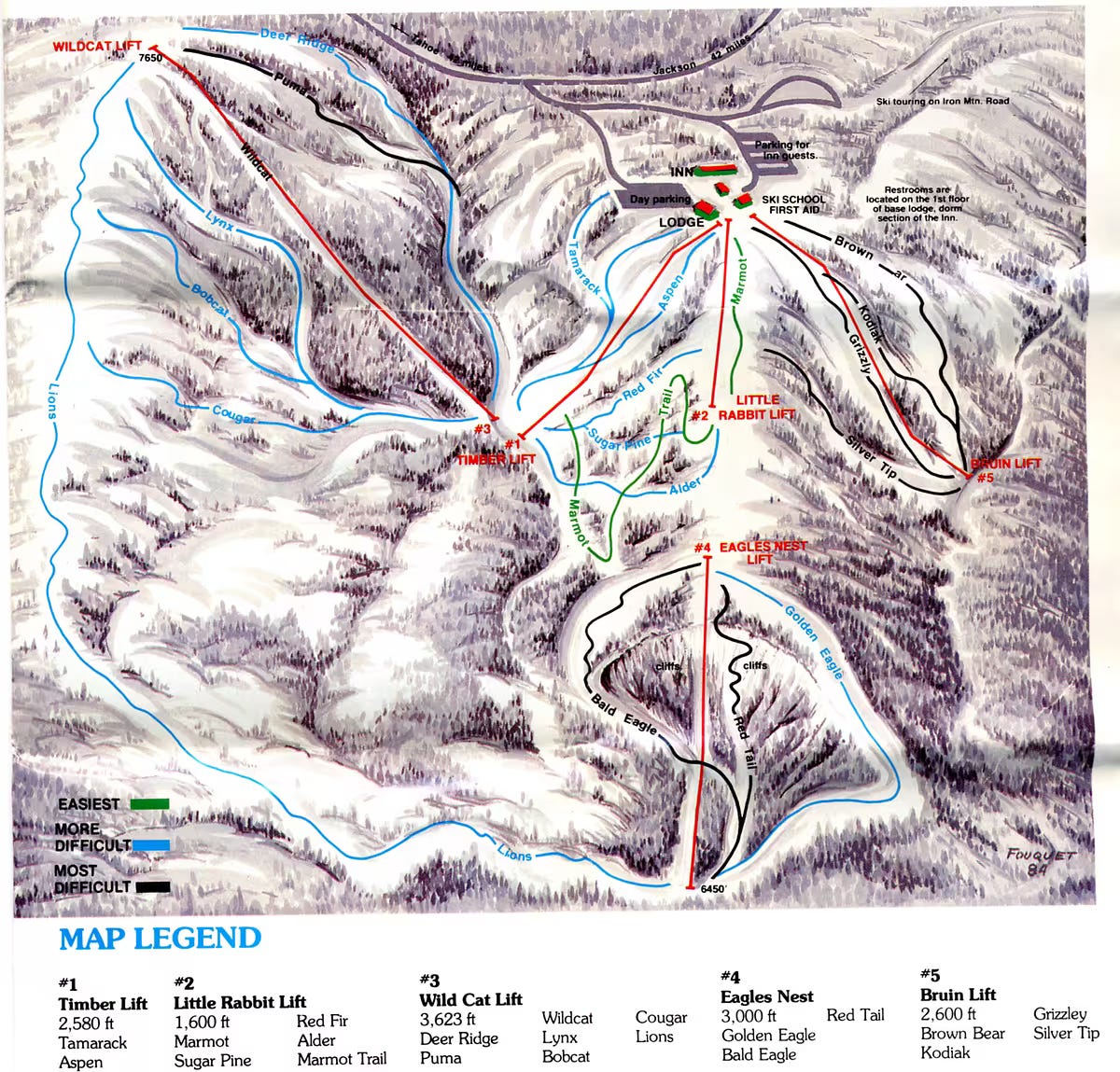

Here’s Iron Mountain’s trailmap, for context - the Wildcat lift rises in the lower right-hand corner of the image above; this was a rare upside-down California ski area, and you can see the parking lots where the blue squiggly line ends (above) at the bottom:

Iron looks to be closer in size to Diamond Peak, which lists 655 acres, so I went with a slightly higher 700 until someone convinces me otherwise. Anyway this is a good watch:

The biggest buzzkill on this list is Ski Rio: 2,150 vertical feet, 900 skiable acres, three chairlifts, and a bunch of surface lifts. With a base elevation of 9,500 feet – higher than nearby Taos - this bump should have been fine.

Here’s what happened (video by the same guy who made the video above; long-time friend of The Storm; sorry Brah that I just subscribed to your YouTube channel five seconds ago, but I’m new to this game because I’m like 150 in internet years):

Here, all of you subscribe to his channel too - each episode focuses on a lost ski area or on an active resort’s history:

Okay so what’s your point?

Yes, there are absolutely fewer lift-served Alpine ski areas in 2025 than there were in 1992. But that’s not the headline. The headline is that the number of lift-served ski areas stabilized around 2000, thanks to advances in snowmaking technology, the mainstreaming of season passes, and better management practices driven, in part, by industry consolidation. And the ski areas that survived have grown to not only replace, but vastly expand, any skiable terrain lost to the shuttered.

I’m struggling to figure out where Crystal’s extra 300 acres came from. The resort has actually contracted a bit during that span as far as I can tell, not expanded (although lift-served access has increased significantly since the old bus-serviced Northback became lift-serviced Northway).

Lower Northway Run down to the old shuttle stop was abandoned after the lift was installed, as was all other terrain below the bottom of the lift, and they abandoned the top section of Boondoggle when Quicksilver was replaced with a shorter lift.

Oddly enough, despite being beyond a ski area boundary sign, Upper Boondoggle actually got groomed a couple times this season, something that never happened when it was still officially inbounds.

Billion Basin also used to be inbounds, but it was abandoned well before 1992, so isn’t relevant here.

The 750 acre increase at Mt. Hood Skibowl, Oregon, can't be right. They did add about 300 acres opening the Outback and added one run (Reynolds), but that was in 1987 and does not add up to a 4X area expansion, https://skibowl.com/about-winter/history/. On the other hand, I think you missed two and a half area expansions at Timberline Lodge, Oregon. The first one in 2007 with the Jeff Flood lift and Still Creek Basin, second one with the acquisition of Summit Ski Area in 2018, and the half one when the permit area was expanded in 2021 to cover the area between the two formerly separate areas (the area between the Alpine Trail and West Leg road). https://www.timberlinelodge.com/about-us/history